Weekly market news 06/29/2026

Weekly market news 06/29/2026

- Mongolian Stock Exchange Market Overview.

- Mongolia's central bank keeps policy rate unchanged at 12%.

- Parliament approves comprehensive tax reform package.

- Bayanteeg JSC declares additional dividend.

- Erdene Resource Development Corporation's share registration updated.

- Global tech stocks rocked by broad sell-off.

- US–Iran deal rattles global commodity markets.

- Global Stock Markets Overview.

► MONGOLIAN STOCK EXCHANGE

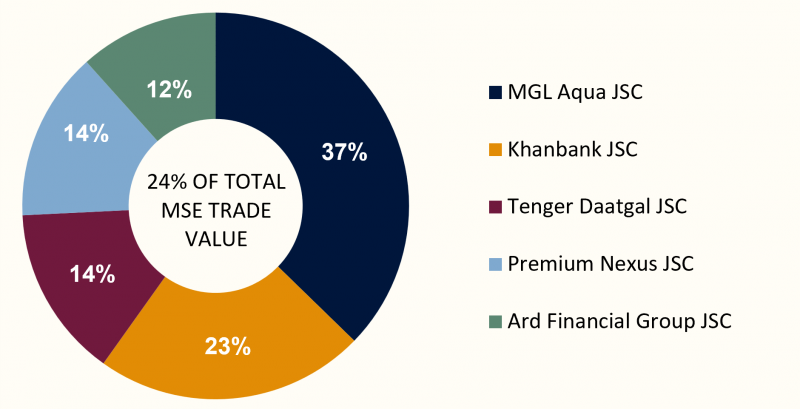

Over the course of the week, a total of 12.4 million securities with a combined value of MNT 18.6 billion were traded on the Mongolian Stock Exchange. In terms of trading value, MGL Aqua JSC, Khan Bank JSC, Tenger Insurance JSC, Premium Nexus JSC, and Ard Financial Group JSC led the market. During the period, one block trade was executed.

- MGL Aqua JSC (MGLA): 5.5 million shares traded at MNT 307 per share, with a total transaction value of MNT 1.7 billion;

- Tenger Insurance JSC (TGI): 625.0 thousand shares traded at MNT 800 per share, totaling MNT 500.0 million;

- Ard Financial Group JSC (AARD): 126.2 thousand shares traded at MNT 3,050 per share, totaling MNT 385.0 million;

- Trade and Development Bank JSC (TDB): 10.0 thousand shares traded at MNT 33,000 per share, totaling MNT 330.0 million;

- Premium Nexus JSC (CUMN): 1.8 million shares traded at MNT 350 per share, with a total transaction value of MNT 636.7 million.

The Mongolian Stock Exchange indices closed with mixed performance. The TOP-20 Index rose by 2.25% to 52,527.04 points, indicating stronger demand for the market's largest listed companies. The MSE A Index also ended higher, suggesting continued buying interest in mid-cap stocks. Meanwhile, the MSE B Index edged lower, reflecting mild profit-taking in smaller-cap companies. The FTI Index declined by 2.83%, indicating weaker performance among investment fund units. Overall, market activity suggests that investor interest remained concentrated in large- and mid-cap stocks, while trading in small-cap companies and investment fund products was more selective.

| INDEX | POINTS | WEEKLY CHANGE |

| TOP 20 Index | 52,527.04 | +2.25% |

| MSE A Index | 19,985.68 | +0.94% |

| MSE B Index | 14,170.14 | -0.18% |

| FTI Index | 1,027.63 | -2.83% |

⇒ MONGOLIA'S CENTRAL BANK KEEPS POLICY RATE UNCHANGED AT 12%

The Monetary Policy Committee of the Bank of Mongolia decided to keep the policy rate unchanged at 12.0% at its June 2026 meeting. The central bank explained that while inflation remains above its target range, recent price increases have been driven primarily by supply-side factors, whereas domestic demand and activity in non-mining sectors remain relatively subdued.

- Policy Rate: 12.0% (unchanged)

- Annual Inflation: 11.2% nationwide; 11.0% in Ulaanbaatar

- Q1 2026 GDP Growth: 7.9%

- Medium-Term Target: Inflation to stabilize at 5% ±2 percentage points from 2027

According to the Bank of Mongolia, the recent acceleration in inflation has been largely driven by higher fuel and food prices. At the same time, core inflation has remained relatively stable, and domestic demand pressures have not increased significantly, leading the central bank to view the current rise in inflation as largely temporary. Inflation is expected to gradually moderate over the medium term as food and fuel price pressures ease. However, the Bank noted that geopolitical tensions in the Middle East and the Russia–Ukraine conflict, adverse weather conditions, and livestock disease outbreaks could prolong supply-side inflationary pressures. It also highlighted that stronger-than-expected economic growth in China is supporting Mongolia's export outlook, while elevated global gold and copper prices continue to improve the country's terms of trade. Nevertheless, higher global energy prices remain an upside risk to inflation.

From a capital markets perspective, maintaining the policy rate signals continued monetary policy stability. However, with inflation still above target, financing costs are expected to remain elevated in the near term. Future monetary policy decisions will continue to depend on the inflation outlook, global commodity prices, and developments in both the domestic and international economic environment.

⇒ PARLIAMENT APPROVES COMPREHENSIVE TAX REFORM PACKAGE

During its spring session, the State Great Khural (Parliament) approved amendments to the General Tax Law, the Corporate Income Tax Law, the Personal Income Tax Law, and the Value Added Tax (VAT) Law. Most of the amendments will take effect on 1 January 2027.

- Personal Income Tax (PIT): Monthly income of up to MNT 792,000 will be exempt from personal income tax.

- Corporate Income Tax (CIT): Businesses with annual sales revenue of up to MNT 2.5 billion will qualify for the 1% preferential tax rate.

- Value Added Tax (VAT): The mandatory VAT registration threshold will increase from MNT 50 million to MNT 400 million in annual sales.

- General Tax Law: The period for amending tax returns will be extended to two years, while several restrictions imposed on taxpayers will be eased.

The revised tax package introduces a number of measures aimed at improving tax administration, reducing the tax burden for individuals and businesses, and supporting the growth of small and medium-sized enterprises. The amendments also introduce a taxpayer compliance rating system and extend the period for correcting tax filings to two years, marking a shift toward a more risk-based approach to tax administration.

⇒ BAYANTEEG JSC DECLARES ADDITIONAL DIVIDEND

Bayanteeg JSC's Board of Directors has approved an additional cash dividend of MNT 3,960 per share under Resolution No. 11 dated 5 June 2026, pursuant to Article 46 of the Company Law. Shareholders recorded as of 13 April 2026, the record date for the company's 2026 Annual General Meeting, will be eligible to receive the additional dividend. The company plans to distribute the dividend during the third quarter of 2026.

- Additional Dividend: MNT 3,960 per share

- Record Date: 13 April 2026

- Payment Period: During Q3 2026

From a capital markets perspective, the additional dividend reflects the company's financial capacity and its commitment to returning value to shareholders. Companies with a consistent dividend policy are generally viewed positively by investors, as they can support long-term investor confidence and enhance shareholder returns.

⇒ ERDENE RESOURCE DEVELOPMENT CORPORATION'S SHARE REGISTRATION UPDATED

Pursuant to Resolution No. 421 issued by the Chairman of the Financial Regulatory Commission on 15 June 2026 and Resolution No. A/287 issued by the Chief Executive Officer of the Mongolian Stock Exchange on 17 June 2026, the securities registration of Erdene Resource Development Corporation has been updated. The amendment reflects the addition of 18,334 common shares that were newly listed on the Toronto Stock Exchange (TSX), bringing the company's total registered shares to 65,356,722.

- Newly Registered Shares: 18,334 common shares

- Previous Total Shares: 65,338,388

- Updated Total Shares: 65,356,722

- Reason for Amendment: Registration of additional shares listed on the Toronto Stock Exchange

This type of registration update helps maintain consistency between the company's dual listings and ensures that the official share registry accurately reflects the total number of issued shares across both exchanges.

Global equity markets experienced increased volatility last week as easing geopolitical tensions were offset by continued uncertainty surrounding monetary policy. Lower oil prices improved expectations that global inflationary pressures could moderate, but central banks' commitment to maintaining relatively high interest rates continued to limit investor risk appetite. At the same time, the correction in highly valued AI-related technology stocks continued, with investors increasingly rotating toward defensive sectors and companies with more stable earnings and cash flows.

U.S. STOCK MARKET

- S&P 500: -1.95%

- Dow Jones: +0.62%

- Nasdaq: -4.48%

U.S. equities delivered a mixed performance last week. Although the Federal Reserve kept interest rates unchanged, policymakers reiterated that inflation remains a priority and signaled that additional rate hikes could still be considered if necessary. This continued to weigh on high-growth technology stocks. At the same time, progress toward a U.S.-Iran peace agreement helped ease oil prices and partially reduced inflation concerns. However, investors remained focused on the outlook for monetary policy, with some rotating out of technology stocks into more defensive and value-oriented sectors amid concerns over elevated AI-related valuations.

EUROPEAN STOCK MARKET

- FTSE 100: +0.67%

- STOXX Europe 600: +0.00%

- DAX 40 (Герман): -1.86%

- CAC 40 (Франц): -0.58%

European equity markets were relatively stable last week, although performance varied across the region. Optimism surrounding progress toward a U.S.-Iran peace agreement contributed to lower energy prices and improved expectations that inflationary pressures in Europe could ease, providing support for sectors such as banking and travel. However, export-oriented industrial companies faced pressure amid concerns over global economic growth and weakness in the technology sector. Investors also closely monitored eurozone inflation data and the European Central Bank's policy outlook.

ASIAN STOCK MARKET

- Nikkei 225: -2.40%

- KOSPI: -6.07%

- CSI 300: -1.64%

- SSEC : -1.63%

Asian equity markets came under pressure last week. South Korea experienced significant selling in AI and semiconductor stocks, which weighed heavily on regional equity performance. In Japan, investors continued to assess monetary policy expectations and movements in the yen, while Chinese equities remained affected by ongoing weakness in the property sector and expectations of further economic stimulus. Overall, regional markets remained cautious amid volatility in global technology stocks and the prospect of higher U.S. interest rates for an extended period.

⇒ GLOBAL TECH STOCKS ROCKED BY BROAD SELL-OFF

Technology stocks tumbled across global markets this week in a sweeping sell-off that rattled investors from Asia to Europe and Wall Street, as concerns over stretched AI valuations and rising borrowing costs converged.

Markets fell across the globe as renewed doubts over sky-high AI, chip, and memory stock valuations took hold of investors, with the turbulence starting in Asia, where South Korea's Kospi dropped 10%, led by SK Hynix and Samsung, both losing over 12%, before quickly spreading west. In Europe, the Stoxx 600 shed around 1% while its Technology sub-index fell 3%, with STMicroelectronics and Dutch chipmaker ASMI each sliding more than 7%. On Wall Street, the Nasdaq closed 2.21% lower at 25,587.04, and the S&P 500 fell 1.44% to 7,365.46, though the Dow barely moved at -0.09%, cushioned by gains in defensive names like Walmart, Procter & Gamble, and Johnson & Johnson.

A mix of factors fueled the sell-off. Mounting concerns over stretched AI valuations and the prospect of higher U.S. borrowing costs led investors to reassess positions in heavily bid-up names. Market sentiment was also hurt by SpaceX, which slid for several days after its blistering June 12 debut on the U.S. market, with shares briefly dipping below their $150 IPO price before recovering. Not all corners of the market suffered equally.

Despite the volatility, many analysts cautioned against overreaction. Tom Hulick, CEO of Strategy Asset Managers, told CNBC that he was not concerned about a looming catastrophe, noting that "there's too much liquidity out there, and the earnings momentum is very strong right now." Wedbush's Dan Ives echoed that view, framing the episode as one of many "gut check moments" for tech stocks, adding that the AI revolution remains in its early innings.

For now, markets appear to be digesting a reality check rather than a structural breakdown, though investors will be watching closely for signals from upcoming earnings reports to determine whether the recent surge in tech valuations can be sustained.

⇒ US–IRAN DEAL RATTLES GLOBAL COMMODITY MARKETS

The current commodity turbulence traces back to February 28, 2026, when the US and Israel launched joint airstrikes on Iran, triggering Iran's closure of the Strait of Hormuz. The International Energy Agency characterized the disruption as the "largest supply disruption in the history of the global oil market," echoing the 1970s energy crisis through acute supply shortages, currency volatility, and heightened risks of stagflation and recession. Brent crude surged more than 50% during the conflict, briefly exceeding $120 per barrel and sending inflationary shockwaves across the global economy.

After months of intense multilateral negotiations, a breakthrough came on June 17, when Trump and Iranian President Masoud Pezeshkian remotely signed the "Islamabad Memorandum" — a framework establishing a 60-day ceasefire, reopening the Strait of Hormuz, and committing both sides to negotiate Iran's nuclear program and sanctions relief. The United States simultaneously lifted its naval blockade on Iranian ports, with Trump posting, "Ships of the World, start your engines. Let the oil flow!"

Markets reacted sharply. On June 13 alone, as peace optimism built, WTI crude plunged 6%, with the prospect of restored Strait of Hormuz flows unwinding months of geopolitical risk premium. By this week, Brent had fallen further to $74.73 per barrel, while gold dropped below $4,000 per ounce for the first time since November 2025 — declining 3.4% to $3,978.67 — pressured by a strengthening US dollar and rising expectations of prolonged high interest rates.

However, Goldman Sachs warned that oil could still exceed $130 per barrel by year-end if the Strait of Hormuz fails to reopen fully, citing low inventory levels and lingering damage to Gulf infrastructure from the conflict. With Iran's nuclear program still unresolved and Israel operating outside the ceasefire's terms in Lebanon, markets remain one headline away from a sharp reversal.