Weekly market news 06/22/2026

Weekly market news 06/22/2026

- Mongolian Stock Exchange Market Overview.

- Securities market turnover surges 2.4 times, driven by primary market activity.

- MNT remained relatively stable but weakened against major currencies.

- Mongolia ranks 67th in the 2026 world competitiveness ranking.

- Federal reserve holds interest rates steady, reaffirms commitment to fighting inflation.

- Oil prices decline as markets expect easing inflationary pressures.

- Global Stock Markets Overview .

► MONGOLIAN STOCK EXCHANGE

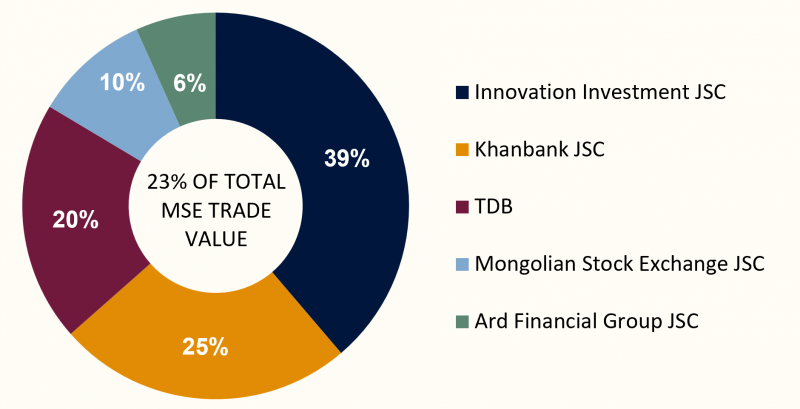

Over the course of the week, a total of 5.3 million securities with a combined value of MNT 7.7 billion were traded on the Mongolian Stock Exchange.In terms of trading value, Innovation Investment JSC, Khan Bank JSC, Trade and Development Bank, Mongolian Stock Exchange JSC, and Ard Financial Group JSC led the market. During the period, one block trade was executed.

- Innovation Investment JSC (QPAY): 2.4 million shares were traded at MNT 271 per share, totaling MNT 650.4 million.

The Mongolian Stock Exchange indices closed with mixed performance last week. The TOP-20 Index declined by 0.09% to 51,371.42 points, suggesting profit-taking in large-cap stocks. In contrast, the MSE A Index gained 0.48% and the MSE B Index rose 0.11%, indicating continued investor interest in mid- and small-cap companies. Meanwhile, the FTI Index advanced 1.28% to 1,057.61 points, reflecting positive performance in investment fund units.

Overall, market activity suggests that investors are becoming more selective, gradually shifting their focus from large-cap stocks toward mid- and small-cap companies as well as investment fund products. The mixed index performance indicates that the market is experiencing sector and product rotation rather than broad-based selling, with trading conditions remaining relatively stable.

| INDEX | POINTS | WEEKLY CHANGE |

| TOP 20 Index | 51,371.42 | -0.09% |

| MSE A Index | 19,800.53 | +0.48% |

| MSE B Index | 14,195.10 | +0.11% |

| FTI Index | 1,057.61 | +1.28% |

⇒ SECURITIES MARKET TURNOVER SURGES 2.4 TIMES, DRIVEN BY PRIMARY MARKET ACTIVITY

According to preliminary data from the National Statistics Office, Mongolia's total securities market turnover reached MNT 797.5 billion in the first five months of 2026, increasing by MNT 465.1 billion, or 2.4 times, compared with the same period last year. The growth was primarily driven by primary market financing, which accounted for nearly 70% of total trading value.

Key Figures:

- Total securities market turnover: MNT 797.5 billion (+MNT 465.1 billion, 2.4x YoY)

- Primary market turnover: MNT 551.6 billion (69.2% of total turnover)

- Secondary market turnover: MNT 245.9 billion (+0.3% YoY)

- TOP-20 Index: Reached 50,866.82 points, up 1,293.4 points from the same period last year

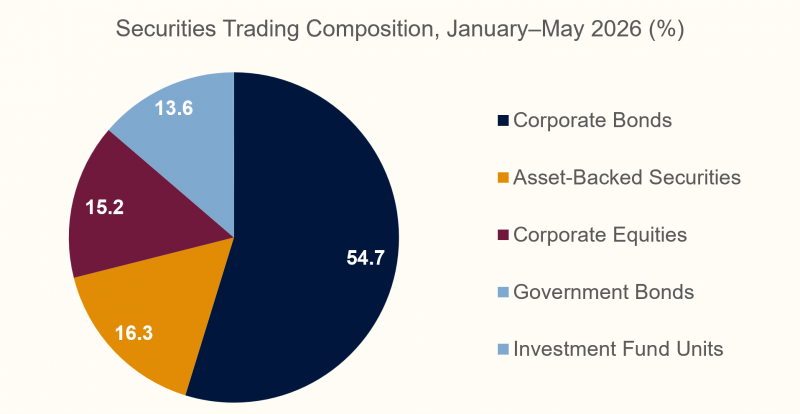

Looking at the composition of trading activity, corporate bonds accounted for 54.7% of total turnover, followed by asset-backed securities (16.3%), corporate equities (15.2%), and government bonds (13.6%). This distribution suggests that investors continue to favor fixed-income instruments, while companies remain actively raising long-term capital through the domestic capital market.

In contrast, the number of securities traded declined by 47.8% year-on-year to 235.4 million units. Trading volume in the secondary market also fell by 48.6%, indicating that the increase in overall turnover was driven primarily by larger primary market transactions rather than stronger secondary market activity. As of May 2026, the total market capitalization of the Mongolian Stock Exchange reached MNT 13.4 trillion, representing a 9.1% increase compared with the same period last year. Meanwhile, the TOP-20 Index gained 149.5 points from the previous month, reflecting steady valuation growth among the market's largest listed companies.

From a capital markets perspective, the strong increase in turnover highlights the growing role of the securities market as a source of corporate financing. However, with most of the growth concentrated in the primary market, secondary market liquidity and trading activity remain relatively subdued, underscoring the need to broaden investor participation and further deepen the domestic capital market.

⇒ MNT REMAINED RELATIVELY STABLE BUT WEAKENED AGAINST MAJOR CURRENCIES

According to the National Statistics Office and the Bank of Mongolia, the Mongolian togrog recorded only modest movements against major foreign currencies in May 2026. The average exchange rate reached MNT 3,576.06 per U.S. dollar, weakening by MNT 3.30 compared with the same period last year and by MNT 2.55 from the previous month. The togrog also depreciated against the Chinese yuan and the Russian ruble, while it appreciated slightly against the euro on a month-over-month basis.

Key Figures:

- U.S. Dollar: 1 USD = MNT 3,576.06 (down MNT 3.30 year-over-year and MNT 2.55 month-over-month)

- Euro: 1 EUR = MNT 4,175.46 (down MNT 144.29 year-over-year but up MNT 1.35 from the previous month)

- Chinese Yuan: 1 CNY = MNT 525.91 (down MNT 30.82 year-over-year and MNT 3.40 month-over-month)

- Russian Ruble: 1 RUB = MNT 48.97 (down MNT 4.65 year-over-year and MNT 2.38 month-over-month)

The recent exchange rate movements suggest that while the togrog continues to experience a gradual depreciation against major trading currencies, the magnitude of the changes remains relatively modest. This indicates that the foreign exchange market has remained broadly stable, with no significant short-term volatility.

At the same time, exchange rate movements continue to have a direct impact on import costs, corporate foreign currency payments, and household spending. In particular, the weaker togrog against the U.S. dollar and the Chinese yuan could place upward pressure on the cost of imported goods, while the slight appreciation against the euro may provide some relief for transactions linked to European markets. Although the currency market has remained relatively stable so far, its outlook will continue to depend largely on export revenues, foreign currency inflows, and developments in global financial markets.

⇒ MONGOLIA RANKS 67TH IN THE 2026 WORLD COMPETITIVENESS RANKING

Mongolia ranked 67th out of 70 economies with a score of 39.02 in the 2026 World Competitiveness Yearbook, published by the World Competitiveness Center in Lausanne, Switzerland. The country slipped two places from last year, when it ranked 65th among 69 economies.

Key Highlights:

- Mongolia ranked 67th out of 70 economies, with an overall score of 39.02.

- Economic performance and government efficiency indicators declined, while business efficiency showed improvement.

- Inflation, policy uncertainty, infrastructure constraints, and limited access to financing were identified as the main factors weighing on competitiveness.

- Foreign direct investment as a share of GDP, merchandise exports, and the proportion of highly educated women remain among Mongolia’s relative strengths.

The report notes that Mongolia continues to face challenges in economic resilience and the competitiveness of its service exports. High inflation, debt pressures, shortages of skilled labor, and weaknesses in logistics and infrastructure remain key obstacles to improving the business environment.

On the positive side, increased investment in education, a growing labor force, and favorable demographic trends are viewed as long-term strengths. Mongolia also maintains relatively strong performance in foreign direct investment relative to GDP and merchandise exports compared with many peer economies.

From a capital markets perspective, the competitiveness ranking is an important indicator used by international investors to assess a country's business environment, institutional quality, and macroeconomic stability. While improvements in business efficiency suggest strengthening private sector activity, persistent challenges related to inflation, policy consistency, and infrastructure development are likely to remain important considerations for long-term investment decisions.

Market performance during the week reflected a transition from geopolitical concerns toward a renewed focus on monetary policy and AI-driven growth. While U.S. and European equities faced headwinds from higher interest rate expectations, Asian markets benefited from easing energy prices and continued strength in semiconductor and AI-related sectors. Overall, sector rotation remains a dominant theme, with investors increasingly favoring selective opportunities rather than broad-based market exposure.

U.S. STOCK MARKET

- S&P 500: -0.22%

- Dow Jones: +0.39%

- Nasdaq: -0.64%

U.S. equities finished the week with mixed performance. Markets rallied at the start of the week after news of a preliminary U.S.-Iran agreement eased concerns over energy prices, pushing the Dow Jones to a record high while AI and semiconductor stocks, including Nvidia and newly listed SpaceX, led gains. However, sentiment weakened after the Federal Reserve kept interest rates unchanged while indicating that another rate hike this year remains possible. Higher Treasury yields weighed on technology and growth stocks, resulting in declines for both the Nasdaq and S&P 500 as investors rotated toward more defensive sectors.

EUROPEAN STOCK MARKET

- FTSE 100: -0.65%

- STOXX Europe 600: -0.17%

- DAX 40 (Герман): +0.37%

- CAC 40 (Франц): -0.48%

European markets also posted mixed results. Early-week optimism driven by lower oil prices and easing Middle East tensions supported airlines, banks, and export-oriented companies, helping Germany's DAX 40 remain in positive territory. Meanwhile, the FTSE 100 and CAC 40 edged lower as investors remained cautious about the economic outlook and future monetary policy, limiting broader market gains.

ASIAN STOCK MARKET

- Nikkei 225: +6.69%

- KOSPI: +6.17%

- CSI 300: +2.33%

- SSEC : +0.91%

Asian markets significantly outperformed their global peers. Lower oil prices benefited import-dependent economies such as Japan and South Korea, while continued optimism surrounding AI infrastructure and semiconductor demand fueled strong gains in technology stocks including Samsung Electronics, SK Hynix, and SoftBank. Chinese equities also ended the week higher, although gains were more modest as investors awaited further policy support and clearer signs of domestic economic recovery.

⇒ FEDERAL RESERVE HOLDS INTEREST RATES STEADY, REAFFIRMS COMMITMENT TO FIGHTING INFLATION

The U.S. Federal Reserve (Fed), under the leadership of its newly appointed Chair Kevin Warsh, decided to keep the federal funds rate unchanged at 3.50%–3.75% during its first monetary policy meeting under his tenure. This marks the fourth consecutive meeting in which the Fed has left interest rates unchanged, reflecting a cautious approach as inflation remains above the central bank's long-term target.

Key Figures

- Federal Funds Rate: 3.50%–3.75% (unchanged)

- May Consumer Price Index (CPI): 4.2% year-over-year

- Federal Reserve Inflation Target: 2.0%

- Updated Outlook: The Fed indicated that one additional rate hike remains possible before the end of 2026.

During his first press conference as Chair, Kevin Warsh emphasized that bringing inflation back under control remains the Federal Reserve's highest priority, stating that "price stability is the foundation of sustainable long-term economic growth." While acknowledging that inflation has remained above the Fed's 2% target for several years, he noted that the recent rise in energy prices should not necessarily be interpreted as a sign of persistently higher long-term inflation.

Under its new leadership, the Federal Reserve also signaled changes to its communication strategy. Compared with previous years, the central bank intends to provide more limited forward guidance and place greater emphasis on a data-dependent approach, making policy decisions based primarily on incoming economic data. In addition, internal working groups will be established to review the Fed's communications framework, balance sheet strategy, and inflation measurement methodologies.

From a capital markets perspective, the decision initially weighed on equity markets, although investors generally welcomed the clearer policy direction. Nevertheless, the Fed's indication that another rate increase remains possible this year is expected to keep U.S. Treasury yields elevated and may contribute to continued volatility in technology and other high-growth stocks. At the same time, expectations that inflation could gradually moderate have preserved market optimism that monetary policy easing may become a possibility in 2027.

⇒ OIL PRICES DECLINE AS MARKETS EXPECT EASING INFLATIONARY PRESSURES

Expectations of a peace agreement between the United States and Iran, along with easing geopolitical tensions in the Middle East, have continued to put downward pressure on global oil prices. Market participants have responded positively to the reduced risk of supply disruptions and the prospect of uninterrupted shipping through the Strait of Hormuz, a key route for global energy trade.

Key Figures

- Brent crude: Down 1.13% to USD 78.65 per barrel

- WTI crude: Down 1.26% to USD 75.82 per barrel

- IEA Outlook: Global oil supply is projected to reach 110.3 million barrels per day in 2027, potentially leading to a supply surplus

- Improved sentiment: Reduced concerns over the Strait of Hormuz have strengthened market confidence in the stability of global oil supply

Oil prices had risen sharply in recent weeks amid heightened geopolitical tensions in the Middle East. However, reports of progress toward a U.S.-Iran peace agreement have prompted markets to reassess geopolitical risks, resulting in a gradual decline in the risk premium previously embedded in crude oil prices.

According to the International Energy Agency (IEA), if current conditions remain stable, increased production from both OPEC+ and non-OPEC producers could lead to a global supply surplus in 2027. Such an outcome would help moderate energy prices and ease inflationary pressures across major economies. Despite the recent decline, analysts remain cautious. Oil prices are still above pre-conflict levels, while rebuilding strategic petroleum reserves and fully normalizing global shipping routes are expected to take time. As a result, any renewed escalation of tensions in the Middle East could quickly reintroduce volatility to the energy market.

From a capital markets perspective, lower oil prices could provide support for transportation, manufacturing, and consumer-related sectors by reducing input costs and easing inflation expectations. At the same time, a more favorable inflation outlook may lessen the need for further monetary tightening by central banks, offering potential support for both equity and fixed-income markets. Nevertheless, investors are expected to continue closely monitoring geopolitical developments, as uncertainty in the region remains an important driver of global market sentiment.