Weekly market news 06/15/2026

Weekly market news 06/15/2026

- Mongolian Stock Exchange Market Overview.

- Inflation surpasses 11%.

- Mining remains the key driver of economic growth.

- Foreign exchange reserves surpass usd 7.7 billion.

- South Korea’s stock market: volatility rises amid the AI boom.

- U.S. inflation rises, while uncertainty over interest rate policy persists.

- Global Stock Markets Overview .

► MONGOLIAN STOCK EXCHANGE

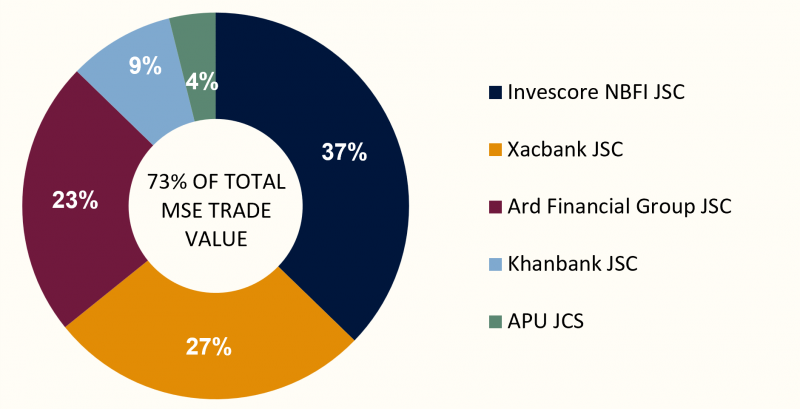

Over the course of the week, a total of 4.9 million securities with a combined value of MNT 6.4 billion were traded on the Mongolian Stock Exchange. In terms of trading value, InvesCore NBFI JSC, Xacbank JSC, Ard Financial Group JSC, Khanbank JSC, and APU JCS were the most actively traded securities during the period. A total of four block trades were executed, including:

- InvesCore NBFI JSC (INV): 104 thousand shares at MNT10,470, totaling MNT 1.1 billion.

- Ard Financial Group JSC (AARD): 188 thousand shares at MNT 3,413, totaling MNT 641 million.

- InvesCore NBFI JSC (INV): 55 thousand shares at MNT 10,950, totaling MNT 602.3 million.

- Ard Financial Group JSC (AARD): 74.3 thousand shares at MNT 5,000, totaling MNT 371.4 million.

Over the past week, the major indices of the Mongolian Stock Exchange closed with mixed performance, while overall market sentiment remained relatively stable. The TOP-20 Index rose by 0.33% to close at 51,415.52 points, while the MSE-A Index gained 1.04% to reach 19,705.42 points, indicating that highly capitalized and actively traded stocks continued to support market growth. In contrast, the MSE-B Index declined by 0.57% to 14,179.79 points, reflecting weaker performance among smaller and less liquid companies. Meanwhile, the newly introduced FTI Index advanced by 1.56% to 1,044.25 points, suggesting stronger momentum within a specific segment of equities and growing investor interest in alternative index products. The FTI (Future Tech Innovation Index) is composed of 17 exchange-traded funds (ETFs) listed on U.S. stock exchanges and is designed to track the performance of sectors such as technology, innovation, energy, and commodities. As a newly launched benchmark, the index provides investors with broader exposure to global growth-oriented industries.

Overall, index performance suggests that market gains remained concentrated in large-cap, higher-quality stocks, while other segments of the market continued to exhibit relatively subdued performance.

| INDEX | POINTS | WEEKLY CHANGE |

| TOP 20 Index | 51,415.52 | +0.33% |

| MSE A Index | 19,705.42 | +1.04% |

| MSE B Index | 14,179.79 | -0.57% |

| FTI Index | 1,044.25 | +1.56% |

⇒ INFLATION SURPASSES 11%

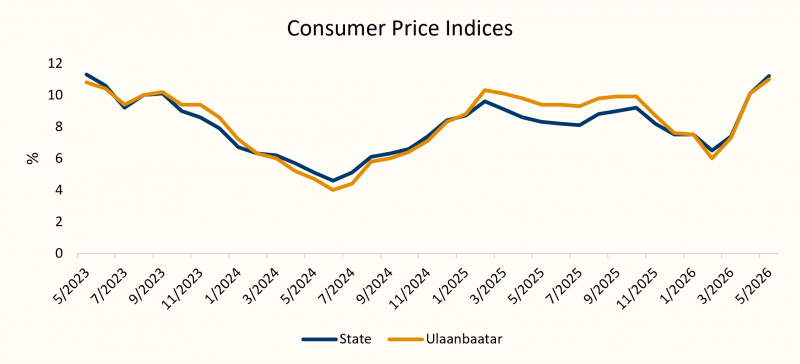

The Consumer Price Index (CPI) has increased for two consecutive months, reaching 11.2% nationwide and 11.0% in Ulaanbaatar in May 2026. This marks the highest inflation rate recorded in the past three years.

Of the nationwide inflation rate of 11.2%, food, beverages, and water accounted for 6.4 percentage points, representing 57.3% of total inflation. Within this category, rising prices of meat and meat products alone contributed 4.4 percentage points to overall inflation, while increases in the prices of domestically produced goods accounted for 3.9 percentage points. In contrast, the impact of gasoline, fuel, solid fuels, and imported goods remained relatively stable.

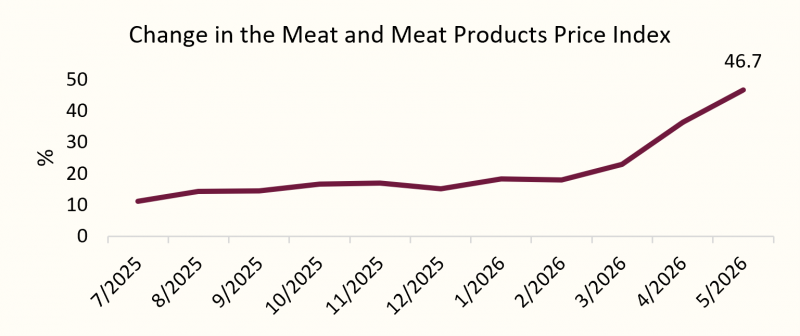

Compared with the same period last year, prices of meat and meat products increased by 46.7%, while prices of bread, flour, and rice rose by 9.4%.

As of May 2026, the average retail price of beef reached MNT 36,257 per kilogram, representing a 55.1% increase from a year earlier. Meanwhile, the price of Grade I flour rose by 11.2% year-on-year to MNT 2,507 per kilogram, while the price of AI-92 gasoline increased by 6.2% to MNT 2,590 per liter.

The sharp rise in meat prices continues to be the primary driver of inflation, highlighting the significant influence of food prices on Mongolia’s overall inflation dynamics.

⇒ MINING REMAINS THE KEY DRIVER OF ECONOMIC GROWTH

Mongolia’s economy expanded by 7.8% year-on-year during the first four months of 2026. The growth was primarily driven by a 30% increase in value added from the mining and quarrying sector. By sector, mining contributed 4.0 percentage points to overall economic growth, while the services sector and agriculture contributed 2.1 and 1.3 percentage points, respectively.

According to the Government’s projections, Mongolia’s real GDP growth is expected to reach 5.7% in 2026, with nominal GDP surpassing MNT 100 trillion. International financial institutions also expect economic growth to remain stable within the range of 5.0%–5.5% in the near term. The projected growth rates for 2026 are 5.5% by the European Bank for Reconstruction and Development (EBRD), 5.0% by the World Bank, and 5.1% by the Asian Development Bank (ADB).

The mining sector continues to serve as the primary engine of economic growth. As such, coal export volumes and the outlook for demand from China are expected to play a decisive role in Mongolia’s economic performance throughout 2026.

⇒ FOREIGN EXCHANGE RESERVES SURPASS USD 7.7 BILLION

Mongolia’s official foreign exchange reserves reached a record high of USD 7.73 billion as of the end of May 2026. This represents an increase of USD 727.8 million, or 10.4%, since the beginning of the year and a rise of USD 406.0 million, or 5.5%, compared to the previous month.

The growth in reserves was primarily driven by stronger export revenues from mining products and increased foreign funding raised by domestic commercial banks. Higher exports of copper concentrate and coal boosted foreign currency inflows, providing significant support to the central bank’s reserve accumulation.

???? Key highlights:

- Official foreign exchange reserves reached a record USD 7.73 billion.

- Reserve holdings are sufficient to cover 7.3 months of imports of foreign-currency-paid goods.

- Reserves are equivalent to 275% of short-term external debt obligations.

The current reserve position exceeds widely used international adequacy benchmarks and strengthens Mongolia’s external payment capacity and overall financial stability. At present levels, foreign exchange reserves can cover approximately 5.3 months of total goods and services imports, providing an important buffer against external shocks, commodity price volatility, and fluctuations in global financial markets.

While the increase in reserves reflects strong export performance and improved foreign currency inflows, their sustainability will continue to depend largely on mining exports and conditions in global commodity markets. A strong reserve position also supports exchange rate stability and reinforces investor confidence in Mongolia’s macroeconomic outlook.

Global equity markets experienced a highly volatile trading week. At the start of the week, U.S. and Asian markets climbed to elevated valuations, supported by continued strength in the technology sector, while European markets also delivered relatively positive performance. However, sentiment shifted later in the week as stronger-than-expected U.S. labor market data reinforced expectations that interest rates could remain higher for longer. This triggered a sharp selloff in U.S. equities and weighed on global markets. Technology and semiconductor stocks were particularly volatile, reflecting investor sensitivity to both interest rate expectations and the outlook for AI-related spending. Overall, the strong gains seen earlier in the week faded as changing macroeconomic expectations reshaped market sentiment. The week ultimately marked a shift from optimism toward a more cautious stance among investors.

U.S. STOCK MARKET

- S&P 500: -0.12%

- Dow Jones: +0.40%

- Nasdaq: -0.68%

Last week, U.S. equity markets closed with mixed performance, while overall market sentiment remained uncertain. The Dow Jones Industrial Average rose by 0.40%, ending the week on a positive note. In contrast, the broader S&P 500 Index declined by 0.12%, while the technology-heavy Nasdaq Composite fell by 0.68%, reflecting a partial rotation of gains away from the technology sector toward other segments of the market. Investors remained focused on the Federal Reserve’s monetary policy outlook, inflation data, and labor market indicators. At the same time, ongoing geopolitical tensions in the Middle East and fluctuations in oil prices continued to weigh on risk sentiment and market volatility. Overall, while markets remained broadly stable, there was a noticeable shift in investor preference away from high-valuation technology stocks toward more defensive and traditional sectors.

EUROPEAN STOCK MARKET

- FTSE 100: +0.99%

- STOXX Europe 600: +2.03%

- DAX 40 (Герман): +0.77%

- CAC 40 (Франц): +2.67%

Last week, European equity markets closed in positive territory. The FTSE 100 Index in the United Kingdom rose by 0.99% over the week, while the STOXX Europe 600 Index, which serves as a broad regional benchmark, gained 2.03%. France’s CAC 40 Index led major benchmarks with a 2.67% increase, while Germany’s DAX 40 Index also advanced by 0.77%, ending the week on a positive note. Market gains were primarily driven by optimistic expectations surrounding U.S.–Iran peace negotiations, a decline in oil prices, and strength in travel and industrial sector equities. On the other hand, the European Central Bank’s 25 basis point interest rate hike had limited impact on sentiment, as the move had largely been anticipated by market participants. Overall, European markets remained relatively stable compared to other global regions, with investors positively reassessing easing geopolitical risks. This contributed to a broadly supportive environment for equity gains throughout the week.

ASIAN STOCK MARKET

- Nikkei 225: +0.11%

- KOSPI: +0.94%

- CSI 300: +1.56%

- SSEC : +2.36%

Asian equity markets closed the week lower across the board. Japan's Nikkei 225 was the most resilient of the region, opening the week at 66,629.6 and closing at 66,588.12, a modest decline of just 0.06%, suggesting that Japanese equities largely weathered the week's global turbulence. South Korea's KOSPI saw the sharpest weekly loss in the region, falling 3.83% from 8,485.67 to close at 8,160.59, likely reflecting the index's heavy weighting toward semiconductor and technology stocks, which came under significant pressure globally following Broadcom's disappointing AI chip outlook and the broader selloff in the tech sector. Chinese markets also ended the week in negative territory, with the CSI 300 declining 1.65% from 4,897.9 to close at 4,816.92, and the SSEC slipping 0.97% from 4,067.16 to 4,027.74, consistent with the cautious global sentiment driven by rising U.S. Treasury yields and fading expectations of Federal Reserve rate cuts in 2026.

⇒ SOUTH KOREA’S STOCK MARKET: VOLATILITY RISES AMID THE AI BOOM

South Korea’s stock market was one of Asia’s best-performing markets during the first half of 2026. Driven by strong demand for AI infrastructure and a global shortage of memory chips, Samsung Electronics and SK Hynix both surpassed a market capitalization of USD 1 trillion, while the KOSPI index rose by more than 100% from the start of the year at its peak. Goldman Sachs projected earnings growth of 300% for 2026, marking the strongest outlook since the recovery from the Asian Financial Crisis in 1999. In short, South Korea became a focal point for global investors.

However, the rally did not last. Stronger-than-expected U.S. employment data reignited concerns that the Federal Reserve could keep interest rates higher for longer, triggering profit-taking across global equity markets. At the same time, investors became increasingly cautious about the sustainability of the AI investment cycle, putting pressure on technology stocks.

The KOSPI closed at 7,484.41, wiping out all of its gains for the week. The selloff accelerated after Broadcom indicated that it would not raise its AI chip targets, prompting a broader retreat in global technology stocks. Foreign investors had sold a cumulative USD 62 billion worth of South Korean equities through the end of May, while margin debt among retail investors climbed to a record KRW 60 trillion, equivalent to roughly USD 39 billion, further amplifying the market correction.

The market later stabilized as investors reassessed the long-term growth prospects of artificial intelligence and the semiconductor sector. Beginning June 10, the KOSPI rebounded sharply, rising 8.18% to close at 8,097. The recovery suggests that investors continue to believe in the long-term AI growth story, even as they balance near-term macroeconomic risks against the sector’s future potential.

⇒ U.S. INFLATION RISES, WHILE UNCERTAINTY OVER INTEREST RATE POLICY PERSISTS

This week’s inflation report attracted significant attention from both financial markets and policymakers. The Consumer Price Index (CPI) rose 4.2% year-over-year in May, marking an increase from previous months. Meanwhile, core inflation—which excludes food and energy prices—remained at 2.9%, suggesting that underlying price pressures have stayed relatively stable.

The increase in inflation was largely driven by higher energy prices. In May, energy costs rose 3.9% from the previous month, while gasoline prices increased 7% month-over-month and more than 40% compared with a year earlier. Market participants continue to point to geopolitical risks affecting global oil supplies, particularly developments in the Middle East, as a key factor behind elevated energy prices.

???? Key Highlights:

- U.S. CPI increased 4.2% year-over-year in May.

- Core inflation remained at 2.9%, indicating relatively stable underlying price pressures.

- Energy prices rose 3.9% during the month, with gasoline prices continuing to be a major contributor to inflation.

From a monetary policy perspective, markets largely expect the Federal Reserve to keep interest rates unchanged in the near term. Inflation remains above the Fed’s target, while the labor market continues to show resilience, increasing the likelihood that any rate cuts could be delayed. As a result, investors are paying close attention to upcoming inflation, employment, and economic growth data.

If interest rates remain elevated for an extended period, growth-oriented and technology stocks could face additional valuation pressure. On the other hand, energy and oil-related companies may benefit from higher commodity prices. However, if wage growth continues to lag inflation, household purchasing power could weaken, potentially weighing on consumer spending and creating challenges for retailers and consumer-focused businesses.

Looking ahead, ongoing uncertainty surrounding developments in Iran and the broader Middle East could continue to influence energy markets and investor sentiment. The pace at which geopolitical tensions ease or escalate will likely remain an important factor shaping market expectations throughout the remainder of 2026.