Weekly market news 06/02/2026

Weekly market news 06/02/2026

- Mongolian Stock Exchange Overview

- The process for inheriting Erdenes Tavan Tolgoi JSC’s 1,072 shares and related dividend entitlements is set to commence.

- The economy expanded by 7.9%, accompanied by improvements in labor productivity.

- The mining sector accounted for 28.6% of total government budget revenue.

- The rapid growth of artificial intelligence (AI) propelled global equity markets to new record highs.

- Positive developments in U.S.–Iran relations contributed to lower oil prices and supported broader financial markets.

- Global Capital Markets Overview.

► MONGOLIAN STOCK EXCHANGE

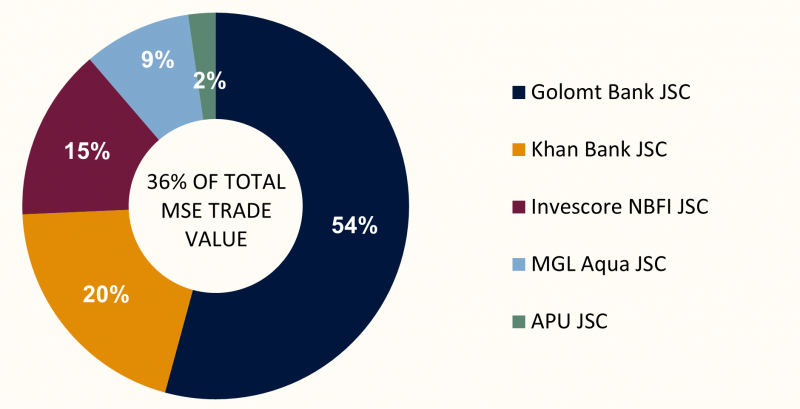

Over the course of the week, a total of 11.42 million securities with a combined value of MNT 14.91 billion were traded on the Mongolian Stock Exchange. In terms of trading value, Golomt Bank JSC, Khan Bank JSC, InvesCore NBFI JSC, MGL Aqua JSC, and APU JSC were the most actively traded securities during the period. A total of three block trades were executed, including:

- MGL Aqua JSC (MGLA): 1.9 million shares at MNT 250, totaling MNT 483.7 million.

- InvesCore NBFI JSC (INV): 67.8 thousand shares at MNT 9,500, totaling MNT 644.7 million.

- Golomt Bank JSC (GLMT): 2.2 million shares at MNT 1,275, totaling MNT 2.78 billion.

Last week, Mongolia’s major stock market indices all closed higher, reflecting continued positive market sentiment. The TOP-20 Index rose 0.78% to 51,360.15 points, while the MSE A Index gained 1.72%, indicating strong buying interest in large- and mid-cap stocks. Meanwhile, the MSE B Index edged up by 0.02%, suggesting relatively stable trading activity among small-cap companies.

The performance of the indices suggests that market gains were primarily driven by larger, more liquid stocks. The stronger performance of the MSE A Index relative to the TOP-20 indicates that investors increasingly favored companies with stronger fundamentals and more stable financial performance. In contrast, capital inflows into the small-cap segment remained relatively limited. Overall, market sentiment remained constructive; however, gains were not broad-based across all sectors and market segments, with investors continuing to adopt a more selective approach.

| INDEX | POINTS | WEEKLY CHANGE |

| TOP 20 Index | 51,360.15 | +0.78% |

| MSE A Index | 19,722.66 | +1.72% |

| MSE B Index | 14,327.15 | +0.02% |

⇒ THE PROCESS FOR INHERITING ERDENES TAVAN TOLGOI JSC'S 1,072 SHARES AND RELATED DIVIDENDS TO COMMENCE

Pursuant to a Government of Mongolia resolution dated 29 April 2026, the transfer of Erdenes Tavan Tolgoi JSC's 1,072 shares and the associated dividend entitlements to lawful heirs will commence on 1 June 2026.

The resolution establishes a legal framework for transferring shares and accumulated dividends belonging to deceased shareholders of Erdenes Tavan Tolgoi JSC who passed away after 31 March 2011 to their lawful heirs. More than 132,000 individuals are expected to be eligible under the inheritance process.

???? Key Steps in the Inheritance Process

- To verify whether a deceased individual held Erdenes Tavan Tolgoi shares, citizens may send the deceased person's registration number via SMS to the dedicated number 158989 using uppercase Cyrillic characters.

- Heirs must prepare the required documentation, including the deceased's death certificate, a residency confirmation issued by the governor of the relevant khoroo or bagh, and a copy of the household registration record. Where inheritance rights arise under Articles 520.1.2 and 520.2 of the Civil Code, heirs may also be required to obtain a family relationship certificate from the General Authority for State Registration.

- Depending on the relationship with the deceased, heirs must provide supporting documentation to establish their legal entitlement. For example, children must submit a birth certificate or birth registration extract, spouses must provide a marriage registration certificate, and parents must provide relevant registration and family relationship documents.

- If any lawful heir chooses to waive their inheritance rights, a notarized waiver must be submitted. Once all required documents have been completed, a notary will issue a Certificate of Inheritance Rights and register the information through the electronic notarial system in accordance with applicable legislation.

Following verification, the Mongolian Central Securities Depository will transfer and register the shares and accumulated dividends into the securities account of the lawful heir.

From a capital markets perspective, the decision is expected to improve the accuracy of Erdenes Tavan Tolgoi JSC's shareholder registry by transferring shares and accumulated dividends previously registered under deceased individuals to their rightful owners. This will improve dividend distribution efficiency and enhance the accuracy of shareholder records. While the company's shares remain unavailable for secondary market trading, the resolution represents a positive step toward strengthening corporate governance and improving transparency in shareholder ownership records.

⇒ ECONOMY EXPANDS BY 7.9%, WHILE LABOR PRODUCTIVITY IMPROVES

According to preliminary estimates released by the National Statistics Office, Mongolia’s real GDP (at 2015 constant prices) grew by 7.9% year-on-year in the first quarter of 2026, reaching MNT 6.7 trillion. The mining and quarrying sector remained the primary driver of growth, contributing 5.0 percentage points to overall GDP expansion.

At current prices, GDP reached MNT 22.9 trillion, representing a 31.8% increase compared to the same period last year. Growth was largely supported by a 74.2% increase in value added from the mining sector, while the services sector also contributed positively, expanding by 15.8%.

From an expenditure perspective, export growth continued to support economic expansion. Exports of goods and services increased by 44.8%, with net exports contributing 16.6 percentage points to GDP growth. In contrast, gross capital formation declined by 34.2%, indicating relatively weaker investment activity during the period.

Labor productivity also improved. GDP per employed person reached MNT 4.8 million in the first quarter of 2026, representing an 11.4% year-on-year increase. The mining sector remained the most productive sector in the economy, with value added per employee reaching MNT 12.9 million.

???? Key Highlights

- Real GDP (2015 constant prices): MNT 6.7 trillion (+7.9%)

- Nominal GDP (current prices): MNT 22.9 trillion (+31.8%)

- Mining sector growth: +33.6%

- Exports of goods and services: +44.8%

- GDP per employed person: MNT 4.8 million (+11.4%)

- Labor productivity in the mining sector: MNT 12.9 million (+12.9%)

While the acceleration in economic growth and labor productivity is encouraging, the data indicate that a significant portion of growth continues to be driven by the mining sector, highlighting the economy’s ongoing concentration in extractive industries. From a capital markets perspective, the current environment remains supportive for mining-related companies and their earnings outlook. However, weaker investment activity and slower growth in non-mining sectors suggest that equity market performance outside the mining sector may remain selective.

⇒ MINING SECTOR ACCOUNTS FOR 28.6% OF GOVERNMENT BUDGET REVENUE

According to the Ministry of Industry and Mineral Resources, Mongolia’s mining sector remained the primary driver of economic growth during the first four months of 2026. Mineral exports reached USD 6.6 billion, representing a 62.5% year-on-year increase, while the mining and quarrying sector accounted for 84.3% of total industrial production.

Beyond supporting export earnings, the mining sector continues to play a critical role in government finances. Total consolidated budget revenue reached MNT 10.2 trillion during the first four months of 2026, increasing by 13.8% year-on-year, or approximately MNT 1.2 trillion. Of this amount, revenue generated from the mineral resources sector totaled MNT 2.9 trillion, up 33.6% from the same period last year, accounting for 28.6% of total government budget revenue. This highlights the continued reliance of public finances on mining sector performance.

At the commodity level, Mongolia produced 38.3 million tonnes of coal, 797.6 thousand tonnes of copper concentrate, 2.1 thousand tonnes of molybdenum concentrate, 2.7 tonnes of gold, 2.3 million tonnes of iron ore, 1.1 million tonnes of iron ore concentrate, 124.3 thousand tonnes of fluorspar ore, 52.1 thousand tonnes of fluorspar concentrate, and 33.2 thousand tonnes of zinc concentrate during the first four months of 2026.

Compared with the same period last year:

- Coal production increased by 42.3%

- Copper concentrate production increased by 29.6%

- Iron ore production increased by 44.4%

- Iron ore concentrate production increased by 49.3%

- Gold production increased by 7.8%

Meanwhile:

- Fluorspar ore production declined by 19.8%

- Zinc concentrate production declined by 24.3%

Within the heavy industry sector, Mongolia produced 2,182.7 tonnes of cathode copper, 13,252.6 tonnes of metal billets, and 12,259.0 tonnes of rolled metal products. Production of metal billets and rolled metal products increased by 0.4% and 0.7%, respectively, while cathode copper production declined by 16.4%. This suggests that growth in downstream processing activities continues to lag the pace of growth in mineral extraction.

In the petroleum sector, crude oil production totaled 1.19 million barrels during the first four months of 2026, representing a 6.4% year-on-year decline, indicating that production trends remain uneven across certain commodity categories.

From a capital markets perspective, earnings prospects for mining-related companies remain favorable, supported by strong production growth and export performance. However, over the longer term, progress in downstream processing, value-added production, and commodity diversification is likely to play a more significant role in determining sector valuations and investor interest.

During the final week of May 2026, global equity markets were characterized by improving investor risk appetite, with U.S. and Asian markets leading gains. In the United States, technology stocks associated with artificial intelligence (AI) continued to drive market performance, while in Asia, the South Korean and Japanese markets were supported by strong momentum in the semiconductor sector. In contrast, European markets delivered relatively weaker performance amid ongoing concerns over inflation, interest rate expectations, and geopolitical uncertainty. Overall, investors remained inclined toward risk assets as concerns over a sharp economic slowdown eased and expectations for a more stable geopolitical environment improved.

U.S. STOCK MARKET

- S&P 500: +1.43%

- Dow Jones: +0.90%

- Nasdaq: +2.39%

U.S. equity markets closed higher last week, with the S&P 500 gaining 1.43%, the Dow Jones Industrial Average rising 0.90%, and the Nasdaq advancing 2.39%. Market performance was primarily driven by technology stocks and companies linked to artificial intelligence (AI). Strong earnings results from Nvidia, continued demand for AI infrastructure investment, and positive financial results from technology companies such as Dell supported investor sentiment and increased risk appetite. In addition, easing tensions between the United States and Iran, alongside positive developments regarding potential ceasefire discussions, contributed to lower oil prices and improved expectations for moderating inflation. Market sentiment was further supported by court rulings related to U.S. trade tariffs, which encouraged a more constructive outlook on economic growth.

EUROPEAN STOCK MARKET

- FTSE 100: -0.78%

- STOXX Europe 600: -0.15%

- DAX 40 (Герман): -0.30%

- CAC 40 (Франц): -0.03%

European equity markets experienced a relatively volatile week but remained broadly stable toward month-end. The FTSE 100 declined by 0.78%, while the STOXX Europe 600, DAX 40, and CAC 40 fell by 0.15%, 0.30%, and 0.03%, respectively. Earlier in the week, positive developments surrounding potential diplomatic progress between the United States and Iran helped lift the STOXX Europe 600 Index to its highest level in more than two months, fully recovering losses associated with previous Middle East-related geopolitical concerns. However, market gains were constrained by persistent inflationary pressures, which increased expectations that the European Central Bank may maintain interest rates at elevated levels for longer. Ongoing geopolitical uncertainty and energy price volatility also contributed to investor caution.

ASIAN STOCK MARKET

- Nikkei 225: +4.20%

- KOSPI: +8.01%

- CSI 300: +0.39%

- SSEC : -1.40%

Asian equity markets delivered the strongest regional performance during the week. Japan’s Nikkei 225 advanced 4.20%, South Korea’s KOSPI surged 8.01%, and China’s CSI 300 gained 0.39%, while the Shanghai Composite Index (SSEC) declined 1.40%. The strong performance of South Korea’s KOSPI was driven by gains in artificial intelligence and semiconductor-related companies, supported by increased domestic institutional investment flows. In particular, the announcement that South Korea’s National Pension Service (NPS) intends to increase its allocation to domestic equities provided additional support to the market. Japanese equities also benefited from continued strength in technology and export-oriented companies. In contrast, Chinese markets exhibited mixed performance as investors remained cautious about the pace of economic recovery and ongoing risks within the real estate sector.

⇒ AI-DRIVEN GROWTH PROPELS GLOBAL EQUITY MARKETS TO NEW HIGHS

During the week of 25–31 May 2026, global equity markets were largely driven by strong gains in the technology sector, particularly companies linked to artificial intelligence (AI). U.S. equity markets led the rally, with both the Nasdaq and S&P 500 reaching record highs, reflecting increasing investor confidence and risk appetite.

The market advance was led by semiconductor manufacturers and companies supporting AI infrastructure. Shares of memory-chip producer Micron Technology surged 19% in a single trading session, pushing the company’s market capitalization above USD 1 trillion for the first time. The move highlighted investors’ growing conviction in the long-term growth potential of AI-related technologies and computing demand.

Meanwhile, Dell Technologies reported financial results that exceeded market expectations and raised its full-year revenue and earnings guidance. Following the announcement, the company’s share price rose by more than 30%, underscoring that the benefits of AI adoption extend beyond chip manufacturers to broader technology ecosystems, including data centers, servers, and computing infrastructure providers.

The strength of the technology sector was also reflected in broader market performance. The Nasdaq gained approximately 8% during May, supported by continued evidence that AI adoption is accelerating across industries and contributing to tangible revenue and earnings growth. This has reinforced investor confidence in the sector's long-term outlook.

While some market participants continue to draw comparisons to previous technology-driven market bubbles and remain cautious about elevated valuations, the current cycle is distinguished by strong underlying financial performance and earnings growth among many of the leading AI-related companies. As a result, many analysts view the current rally not as a purely speculative phenomenon, but as the early stages of a new AI-driven bull market supported by structural technological change.

Looking ahead, continued investment in AI development, computing infrastructure, data centers, and semiconductor capacity is expected to remain a key driver of global equity market performance. As demand for computational power and AI applications continues to expand, the technology sector is likely to remain one of the most influential contributors to global market growth.

⇒ POSITIVE SIGNALS IN U.S.–IRAN RELATIONS WEIGH ON OIL PRICES AND SUPPORT FINANCIAL MARKETS

One of the key developments influencing global financial markets last week was the evolving geopolitical situation between the United States and Iran. Reports suggesting potential progress in diplomatic engagement and peace negotiations between the two countries improved market sentiment and had a notable impact on global energy markets.

In particular, expectations that risks to global oil supply could ease contributed to a sharp decline in crude oil prices. Brent crude fell by approximately 5% in a single trading session, as investors assessed a reduced likelihood of disruptions to energy flows through the Strait of Hormuz, one of the world's most strategically important oil shipping routes.

For the week as a whole, oil prices declined by approximately 9%, providing a supportive backdrop for the global economy. Lower energy prices help alleviate inflationary pressures and may reduce concerns regarding the future path of monetary policy. As a result, investor sentiment toward risk assets improved, supporting gains across major equity markets.

However, geopolitical risks have not been fully resolved. Throughout the week, reports emerged regarding certain U.S. military activities related to regional security operations, highlighting that underlying tensions in the Middle East remain present. Consequently, while markets responded positively to recent developments, uncertainty surrounding the region continues to warrant close attention.

Looking ahead, developments in U.S.–Iran relations, broader geopolitical conditions in the Middle East, and global energy supply dynamics are expected to remain important drivers of both oil prices and global financial market performance. Any material change in regional stability could have significant implications for inflation expectations, energy markets, and investor risk appetite worldwide.