Weekly market news 05/25/2026

Weekly market news 05/25/2026

- Mongolian Stock Exchange Overview

- Economic growth remains heavily driven by mining and market financing.

- Fiscal revenue continues to rise, but the budget deficit has widened to MNT 1.4 trillion.

- The Bank of Mongolia revised reserve requirement regulations on external financing.

- Gold prices remain volatile amid geopolitical risks and high interest rate pressure.

- SpaceX is preparing for what could become the world’s largest IPO.

- Global Capital Markets Overview.

► MONGOLIAN STOCK EXCHANGE

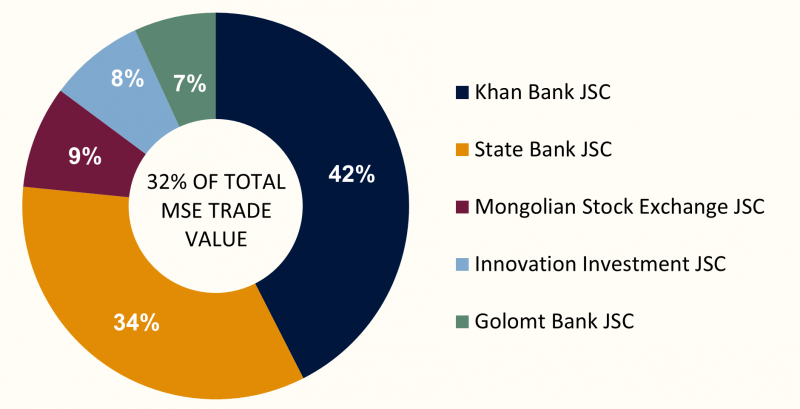

Over the course of the week, a total of 4.9 million securities with a combined value of MNT 4.6 billion were traded on the Mongolian Stock Exchange. In terms of trading value, Khan Bank JSC, State Bank JSC, Mongolian Stock Exchange JSC, Innovation Investment JSC, and Golomt Bank JSC led the market. During the period, a total of one block trade was executed.

- State Bank JSC (SBM): 1 million shares at MNT 442, totaling MNT 442 million.

Last week, the Mongolian Stock Exchange indices closed with mixed performance, reflecting selective buying activity in the market. The TOP-20 Index rose 0.58% to 50,961.19 points, while the MSE B Index gained 0.65%, indicating a moderate recovery in demand for small-cap stocks. In contrast, the MSE A Index declined 0.12%, suggesting relatively stable movement among large- and mid-cap stocks, with profit-taking pressure still present. Market activity suggests that investors are taking a more selective approach and gradually shifting part of their focus from highly liquid blue-chip stocks toward segments with higher growth potential.

| INDEX | POINTS | WEEKLY CHANGE |

| TOP 20 Index | 50,961.19 | +0.58% |

| MSE A Index | 19,389.15 | -0.12% |

| MSE B Index | 14,324.00 | +0.65% |

⇒ ECONOMIC GROWTH REMAINS DRIVEN BY MINING AND CAPITAL MARKET FINANCING

According to the National Statistics Office’s preliminary data for the first four months of 2026, Mongolia’s economic growth continues to be primarily supported by mining, exports, and financial inflows. Total industrial output rose 54.1% year-on-year to MNT 21.8 trillion, while exports increased 60.6% to USD 6.8 billion. At the same time, total securities market turnover more than doubled, reflecting strong financing activity through the capital markets.

Key highlights:

- Total industrial production rose 54.1%, led by 67.5% growth in mining output.

- Securities market turnover reached MNT 563.7 billion, up 2.2x year-on-year.

- Inflation climbed to 10.1%, with food prices rising 19.4%, adding pressure on household consumption.

- GDP grew 8.0% in real terms in Q1 2026, with mining accounting for the majority of the expansion.

Despite strong growth in exports and industrial output, manufacturing growth remained relatively weak at 8.4%, indicating that economic expansion has not been evenly distributed across sectors. The decline in the industrial production volume index also suggests that elevated commodity prices were the primary driver behind nominal growth.

Labor market conditions softened, with the unemployment rate rising to 5.7% while labor force participation declined to 60.4%. Meanwhile, inflation remained in double digits, continuing to weigh on domestic consumption and household purchasing power.

From a capital market perspective, primary market transactions accounted for 65% of total securities turnover, indicating that companies remain actively reliant on the capital markets for fundraising. However, secondary market growth remained relatively subdued, suggesting that liquidity and broader investor participation have yet to fully recover. Earnings expectations for mining-related companies remain strong, while MSE-listed consumer and manufacturing stocks continue to show more selective and uneven performance.

⇒ FISCAL REVENUE CONTINUES TO GROW, BUT BUDGET DEFICIT REACHES MNT 1.4 TRILLION

According to the National Statistics Office’s preliminary data for the first four months of 2026, Mongolia’s consolidated budget revenue and grants reached MNT 10.2 trillion, increasing by 13.8% or MNT 1.2 trillion compared to the same period last year. Meanwhile, balanced revenue and grants totaled MNT 8.9 trillion, up 5.4% year-on-year.

Despite continued revenue growth, total expenditure and net lending reached MNT 10.4 trillion, resulting in a balanced fiscal deficit of MNT 1.4 trillion. This marks a sharp reversal from the surplus recorded during the same period last year and suggests that expenditure growth has begun to outpace revenue expansion.

Key highlights:

- Consolidated budget revenue and grants: MNT 10.2 trillion (+13.8%)

- Balanced revenue: MNT 8.9 trillion (+5.4%)

- Total expenditure and net lending: MNT 10.4 trillion

- Balanced fiscal balance: MNT 1.4 trillion deficit

Total tax revenue reached MNT 8.3 trillion, rising 4.3% year-on-year, mainly supported by a 17.6% increase in social insurance revenue and a 5.8% rise in VAT revenue. In contrast, income tax revenue declined 5.7%, while excise tax revenue fell 28.6%, indicating weaker domestic consumption and softer import activity.

The tax structure shows that 29.9% of total revenue came from income tax, while VAT and social insurance revenue each accounted for 23.4%. At the same time, total fiscal expenditure increased 32.5% compared to the previous year, with both current and capital expenditures rising sharply.

While strong economic growth and mining export revenues continue to support fiscal income, the faster pace of expenditure growth is increasing pressure on the fiscal environment. From a capital market perspective, the widening fiscal deficit could increase the government’s need for domestic bond financing, potentially leading to greater supply of fixed-income instruments in the local market.

⇒ THE BANK OF MONGOLIA REVISED RESERVE REQUIREMENTS ON EXTERNAL FUNDING

The Monetary Policy Committee of the Bank of Mongolia has decided that, starting from October 1, 2026, 25% of foreign currency bonds and loan funding with maturities between 360 days and three years raised from international markets by banks will be included in the reserve requirement base. Previously, these funding sources were fully excluded from reserve requirement calculations, but under the new regulation, only 75% will be exempt, while the remaining 25% will be subject to reserve requirements.

The Bank of Mongolia stated that the measure is aimed at reducing vulnerabilities arising from currency and maturity mismatches within the banking sector, while also limiting excessive reliance on short- and medium-term external funding. The central bank noted that, in developing economies, accumulated currency and maturity mismatches between assets and liabilities can increase systemic financial risks.

Currently, approximately 19% of the banking sector’s total funding consists of external bonds and loans, while the sector’s loan-to-deposit ratio has reached 138%. This indicates that banks have become increasingly dependent on external financing in addition to domestic deposits.

The Bank of Mongolia also noted that recent stress test results showed the banking sector’s capital adequacy would remain at an acceptable system-wide level even under significant macroeconomic shocks. At the same time, non-performing consumer loans have stabilized in recent months, while the volume of loans classified under special attention has begun to decline.

From a capital market perspective, the decision is expected to increase the cost of short-term external funding for banks and encourage greater reliance on domestic funding sources. For MSE-listed banks, investors are likely to focus more closely on funding structures, net interest margins, and external debt exposure going forward.

Last week, global equity markets broadly posted positive performance as investor risk appetite partially recovered. U.S. markets maintained steady gains, while major European and Asian indices recorded stronger advances. Easing geopolitical tensions and the pullback in oil prices from previous highs provided support to global markets. At the same time, expectations surrounding the next steps from major central banks began to stabilize, helping revive investment flows into equities.

U.S. STOCK MARKET

- S&P 500: +0.79%

- Dow Jones: +2.22%

- Nasdaq: +0.81%

In the U.S., the Dow Jones posted the strongest performance, reflecting increased buying interest in industrial, financial, and cyclical sectors. Both the Nasdaq and S&P 500 also closed higher, although momentum in the technology sector appeared more moderate compared to previous weeks. Market sentiment was supported by stabilizing oil prices, easing inflation concerns, and growing expectations that the Federal Reserve’s rate hiking cycle may be nearing its end.

EUROPEAN STOCK MARKET

- FTSE 100: +2.66%

- STOXX Europe 600: +3.43%

- DAX 40 (Герман): +4.43%

- CAC 40 (Франц): +3.24%

European markets delivered the strongest gains of the week. Germany’s DAX 40 rose 4.43%, driven by a rebound in industrial, automotive, and export-oriented sectors. The decline in oil prices from earlier elevated levels helped ease energy cost pressures across Europe and improved the outlook for manufacturers. In addition, expectations that the European Central Bank could adopt a more accommodative policy stance provided further support for equities.

ASIAN STOCK MARKET

- Nikkei 225: +3.33%

- KOSPI: +5.43%

- CSI 300: +0.18%

- SSEC : -0.18%

Asian markets were led by South Korea’s KOSPI, which surged 5.43% amid a strong recovery in technology and semiconductor stocks. Japan’s Nikkei 225 also posted solid gains, supported by yen stabilization and improving expectations for exporters. In contrast, China’s CSI 300 was largely flat while the Shanghai Composite edged lower, reflecting continued weakness in the property sector and lingering uncertainty around domestic demand.

⇒ GOLD PRICES REMAIN VOLATILE AMID GEOPOLITICAL RISKS AND HIGH INTEREST RATE PRESSURE

Global gold markets remained highly volatile over the past week as investors continued to assess geopolitical developments in the Middle East, oil price movements, and the direction of U.S. monetary policy. Spot gold traded around $4,550–4,570 per ounce and remains up more than 35% year-on-year, although prices have undergone a moderate correction over the past month.

One of the key drivers behind gold price movements continues to be uncertainty surrounding the Strait of Hormuz and ongoing U.S.–Iran negotiations. Elevated supply risks in the oil market pushed Brent crude prices sharply higher during 2026, reaching as high as $126 per barrel at one stage. More recently, expectations for renewed peace negotiations helped oil stabilize closer to the $100 level, although markets continue to view supply disruptions as a meaningful risk.

Despite elevated geopolitical tensions, gold has not rallied as aggressively in its traditional safe-haven role. One major reason is that higher oil prices have increased inflation expectations and pushed U.S. Treasury yields higher. Rising bond yields tend to reduce the attractiveness of non-yielding assets such as gold.

Key factors driving the market:

- Uncertainty surrounding the Strait of Hormuz continues to keep oil supply risks elevated.

- Brent crude remains at relatively high levels, contributing to inflationary pressure.

- Higher bond yields are limiting further upside in gold prices.

- Central bank gold purchases and geopolitical risks continue to support long-term demand.

Markets are increasingly focusing less on short-term geopolitical headlines and more on whether the “higher inflation + higher interest rates” environment could persist for longer. This is likely to keep gold markets highly volatile throughout the remainder of 2026.

For Mongolia, elevated global gold prices continue to support export revenues, foreign exchange reserves, and the Bank of Mongolia’s precious metals purchases. However, volatility across commodity markets may also contribute to increased fluctuations in mining-related equities listed on the Mongolian Stock Exchange.

⇒ SPACEX IPO IS POSITIONING TO BECOME THE WORLD’S LARGEST PUBLIC OFFERING

The planned IPOs of major AI and technology companies such as SpaceX, OpenAI, and Anthropic have created significant excitement across global capital markets in 2026. However, some strategists are beginning to warn that the current wave of mega-cap technology IPOs may resemble conditions seen during the peak of the 1999–2000 dot-com bubble.

The most closely watched offering is Elon Musk’s SpaceX, which has become one of the biggest topics in global financial markets. According to market reports, SpaceX is preparing for a Nasdaq listing and could target a valuation of approximately $1.5–1.75 trillion. If achieved, this would make it the largest IPO in financial market history. At the same time, both OpenAI and Anthropic have also announced plans to pursue public listings later in 2026.

A key concern shared by all three companies is that none of them have yet established consistent profitability. SpaceX reported a quarterly net loss of $4.28 billion, while its total loss for 2025 reached $4.94 billion. Approximately 69% of the company’s revenue currently comes from Starlink, while its launch business and AI division remain loss-making. The company’s IPO filings reportedly state that there is no guarantee it will achieve profitability in the future, raising concerns among investors.

One of the most closely monitored developments ahead of the IPO is the progress of the Starship V3 program. SpaceX is aiming to complete successful next-generation Starship test flights before the public offering, as the project is viewed as a critical part of the company’s long-term growth narrative. Starship is expected to play a central role in NASA’s Artemis program, future Mars missions, and broader space infrastructure development.

Some investors believe the largest risk lies in the company’s valuation. At its projected IPO valuation, SpaceX would trade at roughly 67 times revenue, significantly above valuation multiples seen in other mega-cap technology companies such as Nvidia.

Analysts increasingly view the current AI and mega-tech IPO wave not simply as a story of technological innovation, but also as a reflection of renewed investor willingness to assign extremely high valuations based more on future growth potential than current profitability. From a capital markets perspective, the success or failure of these IPOs could have a major impact on technology equity valuations, Nasdaq liquidity flows, and the next cycle of the global AI sector throughout 2026.