Weekly market news 05/18/2026

Weekly market news 05/18/2026

- Overview of trading activity on the Mongolian Stock Exchange

- Securities market turnover surged 2.2x, with the primary market continuing to dominate activity.

- Industrial output rose 54.1%, with the mining sector remaining the main driver of growth.

- The Bank of Mongolia is moving to strengthen its independence while launching reforms aimed at opening up the banking sector.

- The Hormuz crisis is pushing oil prices higher and adding pressure on the U.S. economy.

- The global trade conflict over Chinese EVs is expanding, as the U.S., Canada, and Europe adopt diverging policy approaches.

- Overview of global capital markets

► MONGOLIAN STOCK EXCHANGE

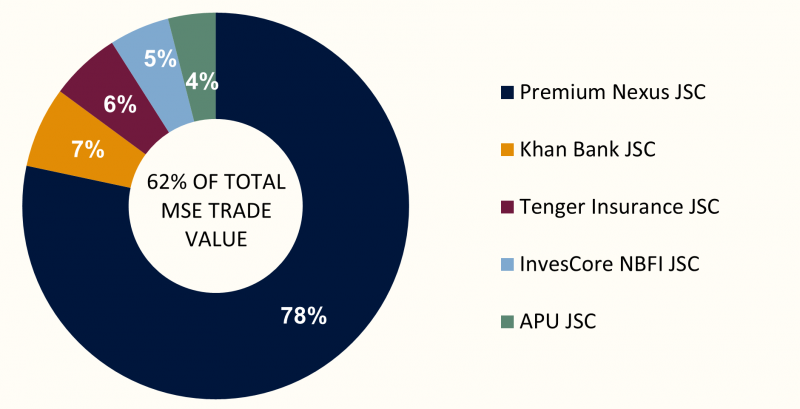

Over the course of the week, a total of 24.18 million securities with a combined value of MNT 13.64 billion were traded on the Mongolian Stock Exchange. In terms of trading value, IPremium Nexus JSC, Khan Bank JSC, Tenger Insurance JSC, InvesCore NBFI JSC, and APU JSC led the market. During the period, a total of three block trades were executed.

- Tenger Insurance JSC (TGI) traded 625 thousand shares at MNT 800 per share, totaling MNT 500 million.

- Premium Nexus JSC (CUMN) traded 19 million shares at MNT 350 per share, amounting to MNT 6.65 billion.

- InvesCore NBFI JSC (INV) traded 62 thousand shares at MNT 6,800 per share, totaling MNT 421 million.

Last week, the Mongolian Stock Exchange’s major indices closed lower as profit-taking following the recent recovery and growing market caution weighed on sentiment. The TOP-20 Index declined 0.33%, the MSE A Index fell 0.50%, and the MSE B Index dropped 0.96%. The sharper decline in the MSE B Index suggests stronger selling pressure in small-cap stocks. While large-cap equities remained relatively stable, activity in the small- and mid-cap segments weakened, with trading volumes slowing compared to previous weeks.

During the week, key market-related developments included the government’s decision to establish a legal framework for inheriting the 1,072 shares of Erdenes Tavan Tolgoi JSC, proposed amendments to tax legislation, and discussions on improving the utilization of foreign loans. These developments remained among the main topics influencing economic and capital market sentiment.

| INDEX | POINTS | WEEKLY CHANGE |

| TOP 20 Index | 50,666.69 | -0.33% |

| MSE A Index | 19,412.39 | -0.50% |

| MSE B Index | 14,232.15 | -0.96% |

⇒ SECURITIES MARKET TURNOVER SURGED 2.2X AS PRIMARY MARKET ACTIVITY CONTINUED TO DOMINATE

According to the National Statistics Office of Mongolia, total turnover in the domestic securities market reached MNT 563.7 billion during the first four months of 2026, increasing by MNT 303.7 billion year-over-year, or 2.2 times. Primary market transactions accounted for 65.5% of total turnover, equivalent to MNT 369.2 billion, indicating that companies and institutions remain actively reliant on capital market financing. Secondary market turnover reached MNT 194.5 billion, posting a modest annual increase of 1.3%.

Key highlights:

- Total securities market turnover: MNT 563.7 billion

- Year-on-year growth: +MNT 303.7 billion / 2.2x

- Primary market turnover: MNT 369.2 billion

- Secondary market turnover: MNT 194.5 billion

- Securities traded: 185.6 million units (-39.0%)

- Total market capitalization: MNT 13.4 trillion (+9.9%)

By asset class, corporate bonds accounted for 47.1% of total trading activity, reflecting continued strong demand for fixed-income instruments. Asset-backed securities represented 20.2% of turnover, while corporate equities and government bonds accounted for 16.8% and 15.8%, respectively.

The total number of securities traded declined 39% year-over-year to 185.6 million units, suggesting that market growth was driven more by large-value transactions and primary market fundraising rather than broad-based trading activity. Liquidity growth in the secondary market remained relatively limited, indicating that wider retail and institutional participation has yet to expand meaningfully.

The TOP-20 Index reached 50,717 points in April 2026, rising compared to the same period last year but declining by 1,710 points from the previous month. This suggests that the market is undergoing a short-term correction following earlier gains. Total market capitalization increased 9.9% year-over-year to MNT 13.4 trillion, although it weakened on a monthly basis.

⇒ INDUSTRIAL OUTPUT ROSE 54.1% AS MINING CONTINUED TO DRIVE GROWTH

According to preliminary data from Mongolia’s National Statistics Office, total industrial output reached MNT 21.8 trillion during the first four months of 2026, marking a 54.1% increase compared to the same period last year. The mining and extractive industries remained the primary growth driver, with sector output rising 67.5% year-over-year to MNT 18.4 trillion.

Metal ore extraction more than doubled, increasing by MNT 6.0 trillion, while coal production rose 25.6%, strongly supporting export revenue and industrial sales. Total industrial sales reached MNT 26.6 trillion, up 79.5% year-over-year, of which MNT 20.4 trillion came from mining export sales.

Key market highlights:

- Metal ore extraction doubled, accelerating mining export growth

- The industrial production volume index declined 15.5%, indicating price effects remained dominant

- Growth in manufacturing activity remained relatively weak

At the product level, coal production increased 54.8%, iron ore output rose 44.4%, iron ore concentrate climbed 49.3%, and copper concentrate production grew 29.6%. In contrast, production of crude oil, silver concentrate, and zinc concentrate declined. Within the manufacturing sector, cement, cashmere products, and combed cashmere production increased, while beverages, meat products, and refined copper cathode production weakened.

The industrial production volume index fell 15.5% year-over-year, suggesting that nominal growth continues to be driven heavily by elevated commodity prices rather than broad-based real production growth. This indicates that while the mining cycle is continuing to support the economy, growth remains uneven across sectors.

Manufacturing output grew only 8.4%, while production of beverages, meat, and copper cathodes declined. This points to relatively weak recovery in domestic consumption and non-mining sectors. On the Mongolian Stock Exchange, consumer and manufacturing-related equities continue to lag behind mining-linked companies in terms of market performance and investor interest.

⇒ BANK OF MONGOLIA PUSHES REFORMS TO STRENGTHEN INDEPENDENCE AND OPEN UP THE BANKING SECTOR

Senior officials at the Bank of Mongolia recently outlined policy priorities related to monetary policy, inflation, banking sector reform, and macroeconomic risks. As inflationary pressure remains elevated, the central bank is focusing on strengthening institutional independence and advancing reforms aimed at liberalizing the banking sector.

Governor S. Narantsogt stated that the central bank’s current independence score stands at around 60%, which he described as insufficient. He noted that amendments to the central bank law are being prepared to reinforce price stability as the institution’s core mandate. The reforms also aim to limit the use of the central bank in quasi-fiscal programs and improve coordination between fiscal and monetary policy.

Within the banking sector, authorities highlighted that banks account for roughly 90% of Mongolia’s financial system, underscoring the need to improve competition and reduce ownership concentration. Proposed revisions to the Banking Law would allow greater participation from foreign banks and international development institutions as shareholders in Mongolian banks, while also creating a more open investment environment.

On inflation, the Bank of Mongolia reported that annual inflation reached 10.1% in April, up 2.7 percentage points from the previous month. Around 2 percentage points of the increase came directly from higher meat and fuel prices. Meat and meat product prices rose 38% year-over-year, while fuel prices increased 17%, making them the largest contributors to inflationary pressure.

The central bank kept the policy rate unchanged at 12%, arguing that the recent inflation spike is largely supply-driven. Officials stated that policy is currently focused more on containing second-round inflation effects and managing inflation expectations rather than responding aggressively with tighter monetary policy. Household 12-month inflation expectations were reported at 7.9%, remaining below the current inflation rate.

The Bank of Mongolia is also studying a gradual transition toward a more market-based mortgage financing system. This includes targeting subsidized 6% mortgage loans more narrowly while expanding mortgage products priced at market rates of 8–12%. At the same time, the central bank continues to prioritize protecting foreign exchange reserves, slowing import-driven consumption growth, and supporting business lending activity.

Global equity markets traded under pressure during the week of May 11–15, 2026, as investors weighed geopolitical risks, rising oil prices, and uncertainty around monetary policy. U.S. equities remained relatively resilient, supported mainly by selective strength in technology stocks, while Europe and Asia saw broader weakness as risk-off sentiment intensified across export- and manufacturing-heavy sectors. The stalled U.S.–Iran negotiations and ongoing uncertainty surrounding the Strait of Hormuz kept oil prices elevated and brought inflation concerns back into focus. Markets increasingly shifted attention beyond interest rate expectations toward supply shocks, energy prices, and geopolitical risks, contributing to widening performance divergence across regions.

U.S. STOCK MARKET

- S&P 500: +0.31%

- Dow Jones: -0.05%

- Nasdaq: +0.34%

U.S. markets traded in a relatively stable but mixed pattern during the week. The S&P 500 and Nasdaq posted modest gains, while the Dow Jones ended slightly lower. Technology shares, particularly AI and semiconductor-related companies, continued to support the Nasdaq, although market momentum slowed compared to previous weeks. Investor sentiment was shaped by concerns over stalled U.S.–Iran negotiations, higher oil prices, and uncertainty surrounding Federal Reserve policy. Brent crude remaining near the $110 level reinforced fears of renewed inflationary pressure. At the same time, U.S. inflation data showed limited improvement, weakening expectations for near-term rate cuts and weighing more heavily on traditional sectors represented in the Dow Jones index.

EUROPEAN STOCK MARKET

- FTSE 100: -0.37%

- STOXX Europe 600: -0.83%

- DAX 40 (Герман): -1.57%

- CAC 40 (Франц): -1.45%

European markets experienced broad-based declines, with Germany’s DAX 40 and France’s CAC 40 posting the steepest losses. The weakness reflected growing risk aversion among investors amid rising geopolitical uncertainty in the Middle East and higher energy prices. Expectations of increasing energy costs pressured Europe’s export-oriented and industrial sectors, particularly in Germany, where automotive and manufacturing stocks weakened notably. In France, the CAC 40 was weighed down by concerns over consumer demand and softer performance in discretionary spending-related sectors.

ASIAN STOCK MARKET

- Nikkei 225: -2.84%

- KOSPI: -3.63%

- CSI 300: -0.87%

- SSEC : -1.57%

Asian markets faced the strongest selling pressure during the week, led by sharp declines in South Korea’s KOSPI and Japan’s Nikkei 225. Chinese indices also moved lower, reflecting weaker investor risk appetite across the region. Technology and export-oriented sectors in Japan and South Korea remained highly sensitive to global demand expectations and developments in the U.S. technology cycle. In Japan, volatility in the yen and renewed discussions surrounding U.S.–Japan currency issues added further uncertainty to the market. In China, concerns over the weak property sector, slowing domestic demand, and the possibility of renewed U.S.–China trade tensions continued to weigh on sentiment.

⇒ HORMUZ CRISIS DRIVES OIL HIGHER AS PRESSURE BUILDS ON THE U.S. ECONOMY

Last week, global markets remained focused on uncertainty surrounding the Strait of Hormuz, stalled U.S.–Iran peace negotiations, and heightened volatility in oil prices. After U.S. President Donald Trump stated that Washington would not accept Iran’s proposed conditions, Brent crude remained above the $110 level, intensifying concerns over potential supply disruptions. During the week, Brent traded between $107–111 per barrel, while WTI crude fluctuated around $102–107.

Tensions escalated further after Iran’s state-affiliated “Fars” news agency published details of five key U.S. demands presented during the second round of negotiations. According to Iranian sources, the U.S.:

- Refused to compensate Iran for war-related damages

- Demanded the transfer of 400 kg of enriched uranium

- Sought to limit Iran to operating only one nuclear facility

- Rejected releasing 25% of Iran’s frozen assets

- Linked a ceasefire directly to progress in negotiation

Iranian officials described the demands as an attempt by the U.S. to achieve through diplomacy what it could not achieve through military action, while Iran’s “Mehr” agency reported that negotiations had reached a “deadlock.” At the same time, Israeli Prime Minister Benjamin Netanyahu stated that operations related to Iran were “not over,” adding to geopolitical uncertainty across global markets.

The U.S. Energy Information Administration (EIA) estimates that ongoing disruption in the Strait of Hormuz could remove 10–14 million barrels per day from global supply. Saudi Aramco CEO Amin Nasser also warned that if conditions in Hormuz do not normalize soon, the global oil market could face a deeper supply shortage.

Rising oil prices are beginning to place additional pressure on the U.S. economy as well. According to CNBC, average U.S. gasoline prices climbed to around $4.5 per gallon, slowing the recent moderation in inflation. This has weakened expectations for Federal Reserve rate cuts and pushed investors toward a more cautious stance. Markets are increasingly shifting their focus from short-term geopolitical volatility toward the risk of a prolonged supply shock, with developments in Hormuz and future U.S.–Iran negotiations likely to remain key drivers of oil prices and global inflation trends.

⇒ GLOBAL TRADE TENSIONS OVER CHINESE EVS ARE ESCALATING AS THE U.S., CANADA, AND EUROPE TAKE DIFFERENT APPROACHES

China’s electric vehicle (EV) exports have surged sharply over the past two years, reshaping the competitive landscape of the global auto industry and prompting the U.S., Canada, Europe, and other countries to strengthen protective trade policies. Chinese manufacturers such as BYD, SAIC, Geely, and Leapmotor have rapidly expanded their global presence through lower pricing, advanced technology, and strong state-backed industrial support, increasing pressure on Western automakers.

UNITED STATES: THE MOST AGGRESSIVE PROTECTIONIST APPROACH

The U.S. has adopted the toughest stance against Chinese EV imports. Washington imposed a 100% tariff on Chinese EVs in 2024, and in 2026 Congress backed the “Connected Vehicle Security Act,” reflecting growing concerns that Chinese vehicles may pose national security risks. U.S. automakers and labor unions have also urged the Trump administration not to open the domestic market to Chinese EV manufacturers.Key U.S. concerns include:

- State-supported low-cost Chinese EVs

- Risks to domestic manufacturing and employment

- Data security and cybersecurity issues linked to connected vehicles

- Expanding North American influence of companies such as BYD

CANADA: PARTIALLY EASING ITS POSITION

Canada initially mirrored the U.S. by imposing a 100% tariff on Chinese EV imports, but shifted its policy in early 2026 by allowing imports of up to 49,000 Chinese EVs annually. In return, China reportedly agreed to reduce tariffs on Canadian canola and agricultural exports.

The move drew criticism from Washington, where officials argued that Chinese EVs could ultimately enter the U.S. market through Canada. U.S. Transportation Secretary Sean Duffy stated that Canada may eventually “regret” the decision.

EUROPE: COMBINING TARIFFS WITH INDUSTRIAL COOPERATION

The European Union has imposed additional tariffs on Chinese EV manufacturers, though it has stopped short of the more restrictive U.S. approach. Since 2024, the European Commission has applied extra duties on EVs produced in China, with some manufacturers facing tariffs exceeding 35%.

At the same time, Europe is increasingly pursuing a hybrid strategy that combines trade protection with industrial cooperation. Stellantis and Leapmotor have agreed to jointly produce EVs in Spain, while Volkswagen secured special tariff arrangements for its China-made Cupra Tavascan model.

Chinese-made EVs continue to gain market share in Europe, accounting for roughly 22% of EV sales during the first four months of 2026.

Outside North America and Europe, countries are responding differently. Turkey imposed either an additional 40% tariff or a minimum $7,000 tax on Chinese vehicles to protect domestic production, while Mexico, Southeast Asia, and parts of Latin America remain more open to Chinese EV investment and imports.

The global EV market is increasingly dividing between two competing policy models: open competition versus industrial protectionism. The U.S. is effectively closing off its market to defend domestic manufacturers, while Europe is attempting to balance tariffs with selective integration of Chinese automakers through localized production. Meanwhile, China continues accelerating exports as domestic competition and excess manufacturing capacity intensify, setting the stage for a prolonged global trade conflict in the automotive sector.