Weekly market news 04/06/2026

Weekly market news 04/06/2026

- Overview of trading activity on the Mongolian Stock Exchange

- Mongolia’s foreign exchange reserves reached a historic high

- Securities market turnover increased by 74.4%, driven by primary market activity

- Gold prices decline as stronger u.s. Dollar and rising oil prices add pressure

- China’s industrial profits rise 15.2% as recovery continues

- Overview of global capital markets

► MONGOLIAN STOCK EXCHANGE

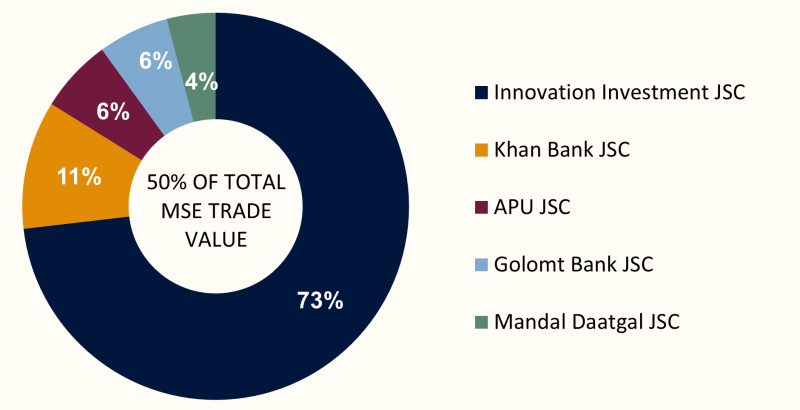

Over the course of the week, a total of 45.55 million securities with a combined value of MNT 24.73 billion were traded on the Mongolian Stock Exchange. In terms of trading value, the most actively traded companies were Innovation investment JSC, Khan Bank JSC, APU JSC, Golomt Bank JSC and Mandal insurance JSC. During the same period, three block trades were executed:

- Invescore NBFI JSC (INV) traded 26.7 thousand shares at MNT 11,110 per share, amounting to MNT 296.6 million in total turnover.

- Tenger insurance JSC (TGI) saw 625 thousand shares traded at MNT 800 per share, generating approximately MNT 500 million in trading value.

- Innovation investment JSC (QPAY) traded 33.1 million shares traded at MNT 270 per share, generating approximately MNT 8.9 billion in trading value.

- Mandal insurance JSC (MNDL) traded 6.6 million shares traded at MNT 75 per share, generating approximately MNT 495 million in trading value.

Over the past week, the Mongolian stock market indices closed lower, indicating broad-based weakness across the market. The TOP-20 Index declined by 2.03%, the MSE A Index fell by 4.66%, and the MSE B Index decreased by 0.75%. The sharper drop in the MSE A Index suggests greater pressure on mid- and large-cap companies.

Market movements during the week were influenced mainly by seasonal factors. As many companies entered their ex-dividend period, share prices adjusted downward for technical reasons, which is a typical pattern during dividend distribution periods. In addition, the announcement of annual general meeting (AGM) schedules and the commencement of shareholder registration had a noticeable impact on short-term investor decisions. Overall, the decline in the indices reflects seasonal and internal market dynamics rather than systemic market risk.

| INDEX | POINTS | WEEKLY CHANGE |

| TOP 20 Index | 51,762.08 | -2.03% |

| MSE A Index | 19,136.73 | -4.66% |

| MSE B Index | 14,486.89 | -0.75% |

⇒ MONGOLIA’S FOREIGN EXCHANGE RESERVES REACHED A HISTORIC HIGH

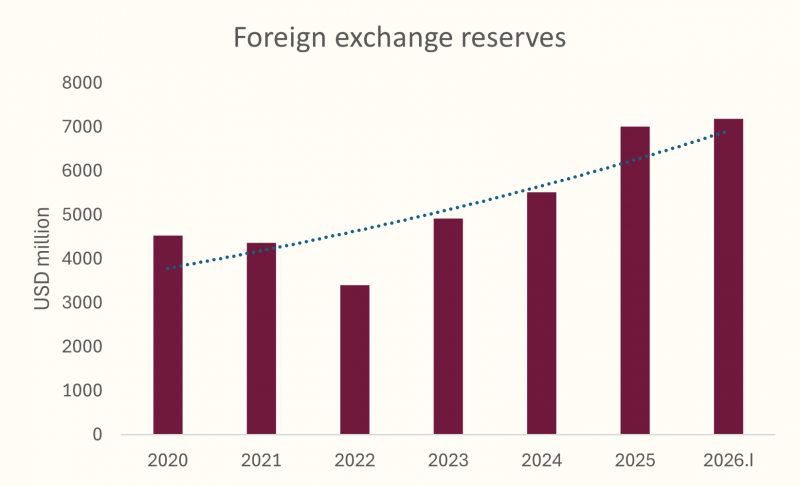

Mongolia’s official foreign exchange reserves reached USD 7.19 billion at the end of the first quarter of 2026, increasing by USD 182.5 million since the beginning of the year and marking a historic high.

This level of reserves indicates a strengthened capacity to maintain external economic balance and meets key international benchmark indicators. Specifically, the reserves are sufficient to cover:

- 8.4 months of imports of goods requiring foreign currency payments

- 5.6 months of total goods and services imports

- 275% of short-term external debt obligations

The rise to a record-high level of foreign exchange reserves is a positive factor supporting macroeconomic stability and enhancing the country’s ability to absorb external shocks. An adequate reserve buffer also helps ease short-term pressures on the MNT exchange rate and the balance of payments.

⇒ SECURITIES MARKET TURNOVER INCREASED BY 74.4%, DRIVEN BY PRIMARY MARKET ACTIVITY

In the first two months of 2026, total turnover in Mongolia’s securities market reached MNT 188.3 billion, increasing by MNT 80.3 billion or 74.4% year-on-year. This growth signals rising market activity, largely supported by a sharp increase in primary market transactions.

Of the total turnover:

56.7% (MNT 106.7 billion) came from the primary market

43.3% (MNT 81.6 billion) came from the secondary market

This indicates that new issuances and financing activities dominated market movements during the period.

Meanwhile, the total number of securities traded fell to 85.0 million units, down 60.6% YoY, suggesting that the increase in turnover was driven not by trading volume but by higher-value instruments.

By structure, total turnover consisted of:

- 41.5% Asset-backed securities

- 23.8% Equities

- 21.6% Government bonds

- 13.0% Corporate bonds

This composition shows that debt instruments continue to hold a significant share of the market.

Market capitalization reached MNT 14.0 trillion as of February 2026, up 4.3% YoY, though down 1.7% month-on-month. Similarly, while the TOP-20 Index increased on a yearly basis, it declined on a monthly basis, indicating a short-term market correction.

Key Indicators

- Total turnover: MNT 188.3 billion (+74.4% YoY)

- Primary market: MNT 106.7 billion (56.7%)

- Secondary market: MNT 81.6 billion (43.3%)

- Securities traded: 85.0 million units (−60.6% YoY)

- Market capitalization: MNT 14.0 trillion (+4.3% YoY)

The sharp rise in turnover reflects increased financing activity in the market and the growing role of the primary market. However, the decline in trading volume suggests a structural shift toward higher-value transactions rather than improved liquidity depth. While overall growth is evident, relatively weak activity in the secondary market remains a factor to watch for sustainable market development.

On a weekly basis, global equity markets posted broad-based gains, marking a recovery phase following the previous decline. Growth was particularly strong in the United States and Europe, while Asian markets showed mostly positive but uneven performance. This suggests that short-term risk sentiment has eased and investor positioning has become more active. However, performance differences across regions remain evident.

U.S. STOCK MARKET

- S&P 500: +2.80%

- Dow Jones: +2.70%

- Nasdaq: +3.71%

The U.S. market delivered positive performance throughout the week, with major indices closing higher. The S&P 500 rose by 2.80%, the Nasdaq Composite gained 3.71%, and the Dow Jones Industrial Average increased by 2.70%. The stronger gain in the Nasdaq indicates that growth and technology stocks led the rebound. Following the previous week’s decline, markets entered a recovery phase as short-term risk aversion eased and buying activity picked up.

EUROPEAN STOCK MARKET

- FTSE 100: +3.04%

- STOXX Europe 600: +3.86%

- DAX 40 (Герман): +4.30%

- CAC 40 (Франц): +3.55%

European markets recorded broad-based gains, with all major regional indices delivering strong performance. The DAX 40 rose by 4.30%, the STOXX Europe 600 gained 3.86%, the CAC 40 increased by 3.55%, and the FTSE 100 advanced 3.04%. This reflects improving risk appetite across the region, with gains supported by broad sector participation rather than being concentrated in a single segment.

ASIAN STOCK MARKET

- Nikkei 225: +2.05%

- KOSPI: +3.77%

- CSI 300: +0.38%

- SSEC : -0.11%

Asian markets were mostly positive during the week. South Korea’s KOSPI rose by 3.77%, while Japan’s Nikkei 225 gained 2.05%, indicating a recovery across key regional markets. In contrast, China’s markets remained relatively weak. The CSI 300 posted only a modest 0.38% gain, while the Shanghai Composite Index declined by 0.11%, reflecting continued uncertainty in the market.

⇒ GOLD PRICES DECLINE AS STRONGER U.S. DOLLAR AND RISING OIL PRICES ADD PRESSURE

Gold prices fell on Thursday as the strengthening U.S. dollar and rising oil prices weighed on the market. Spot gold declined by 3.6% to $4,587.55 per ounce, while U.S. gold futures dropped 2.7% to $4,679.70.

The move followed a statement by Donald Trump regarding the continuation of military actions against Iran, which heightened concerns about rising inflationary pressure and reinforced expectations that interest rates may remain elevated for longer.

A sharp appreciation of the U.S. dollar made gold relatively more expensive for holders of other currencies, dampening demand. At the same time, higher oil prices contributed to inflation concerns, limiting central banks’ room to ease monetary policy.

Although gold is traditionally viewed as a hedge against inflation, it becomes less attractive in a high-interest-rate environment due to its non-yielding nature. As a result, gold prices have fallen by 13% since the conflict related to Iran began on February 28.

Additional pressure came from central bank activity. The Central Bank of the Republic of Türkiye reduced its gold reserves by 69.1 tons to 702.5 tons, with total reductions exceeding 118 tons over the past two weeks.

In Asian markets, gold demand showed mixed trends. In India, falling prices led to gold trading at a premium, while in China, buyers held back in anticipation of further price declines, slightly reducing premiums.

Overall, the decline in gold prices is closely linked to a stronger U.S. dollar and rising oil prices, which have increased inflation and interest rate expectations. Under current conditions, gold appears to be more sensitive to the interest rate environment than serving as a traditional safe-haven asset in the short term.

⇒ CHINA’S INDUSTRIAL PROFITS RISE 15.2% AS RECOVERY CONTINUES

In the first two months of 2026, China’s industrial sector profits increased by 15.2% year-on-year, a sharp acceleration from the 5.3% growth recorded in December 2025. This indicates improving momentum in industrial activity.

According to official data from the National Bureau of Statistics of China, the growth was mainly driven by stronger production activity and rising product prices. High-tech manufacturing led profitability gains, with total profits in the segment rising 58.7%, supported largely by revenue growth among drone and semiconductor manufacturers.

The raw materials sector also showed strong performance, with profits in non-ferrous metals rising 148.2% and the chemical industry up 35.9%.

However, officials emphasized that the recovery remains uneven across sectors, and increasing geopolitical tensions could weigh on the outlook. While disruptions to oil supply in the Middle East have created pressure in global energy markets, China’s impact is expected to be relatively limited due to domestic reserves and alternative energy sources. Continued oil imports from Iran have also helped mitigate risks to some extent.

Overall, the rise in industrial profits reflects improved short-term production activity. Nevertheless, weak domestic demand and uneven sectoral recovery continue to raise questions about the sustainability of growth. Geopolitical risks and energy price volatility remain key factors influencing future performance.