Weekly market news 06/08/2026

Weekly market news 06/08/2026

- Mongolian Stock Exchange Overview

- Efforts to bring the “Borteeg deposit” into economic circulation are intensifying

- From raw fiber to finished goods: Mongolia's cashmere industry gets its biggest push in decades

- Anthropic files for IPO at $965 billion valuation, outpacing OpenAI in race to public markets

- How did the Israel–Lebanon ceasefire affect the oil market?

- Global Capital Markets Overview.

► MONGOLIAN STOCK EXCHANGE

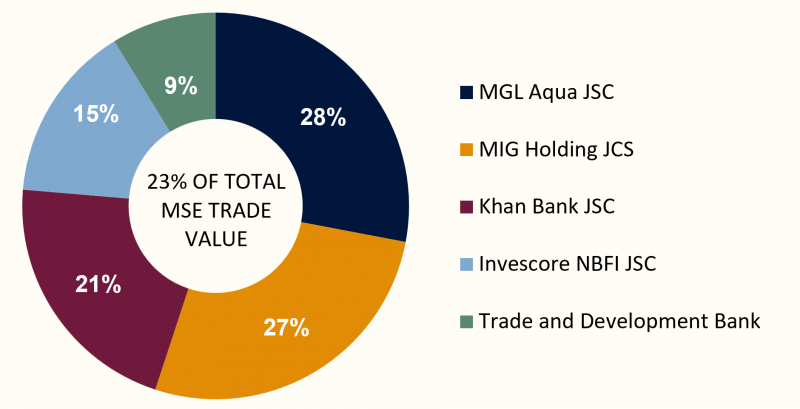

Over the course of the week, a total of 5.96 million securities with a combined value of MNT 11.54 billion were traded on the Mongolian Stock Exchange. In terms of trading value, MGL Aqua JSC, , MIG holding JCS, Khan Bank JSC, InvesCore NBFI JSC, and TDB JCS were the most actively traded securities during the period. A total of three block trades were executed.

- MGL Aqua JSC (MGLA): 2.9 million shares at MNT 250, totaling MNT 749 million.

- InvesCore NBFI JSC (INV): 45.4 thousand shares at MNT 9,500, totaling MNT 369.3 million.

- MIK Holding JCS (MIK): 55.1 thousand shares at MNT 1,275, totaling MNT 725.7 million.

Over the past week, all major indices of the Mongolian Stock Exchange closed lower, as market conditions continued at a relatively stable level. The Top-20 Index declined by 0.02% to close at 51,347.33, while the MSE A Index dropped by 0.80% to 19,565.06, reflecting weakened buying activity among large and mid-cap stocks. The MSE B Index recorded the steepest decline, falling 0.91% to close at 14,196.18, signaling relatively subdued movement in the small-cap segment. Looking at the overall trend, the decline was broadly distributed across all segments, with market activity remaining selective rather than broad-based.

| INDEX | POINTS | WEEKLY CHANGE |

| TOP 20 Index | 51,347.33 | -0.02% |

| MSE A Index | 19,565.06 | -0.80% |

| MSE B Index | 14,196.18 | -0.91% |

⇒ EFFORTS TO BRING THE BORTEEG DEPOSIT INTO ECONOMIC CIRCULATION ARE INTENSIFYING

The Government of Mongolia had set a target to bring the Borteeg coal deposit into economic circulation from 2026, with plans to extract 15 million tons of coal annually and export 10 million tons of that amount. The deposit holds total coal reserves of 424 million tons, of which 95% is semi-coking coal, and the remaining 5% is thermal coal.

As part of implementing the project, the government conducted an open tender for foreign investors, with plans to generate an additional $1 billion in revenue. As a result of the selection process, Erdenes Tavan Tolgoi JSC submitted the highest-rated proposal and was selected to take over management of the Borteeg deposit and carry out extraction in partnership with domestic enterprises.

Under the terms of the agreement, Mongolia's share of returns is calculated at 70%, with the opportunity to receive a total advance payment of $1 billion over the first five years.

Among the other participants in the tender, China's Baowu Resources proposed an advance payment of $600 million with a return share of 51.7%, while China Energy Materials & Technology Xuzhou offered an advance payment of $1 billion but stood out for offering Mongolia a return share of only 51%.

Nevertheless, a notable concern remains: under a previously signed long-term coal supply agreement with China, Mongolia is obligated to supply coal at discounted prices for a period of 16 years. Therefore, even though the tender was won by a Mongolian state-owned company, the risk persists that the actual returns from operating the deposit may be diminished due to the conditions of the prior agreement, and that the Chinese side may retain a more economically advantageous position.

⇒ FROM RAW FIBER TO FINISHED GOODS: MONGOLIA'S CASHMERE INDUSTRY GETS ITS BIGGEST PUSH IN DECADES

Mongolia's economy has long rested on a precarious foundation. Mining accounts for roughly 70% of industrial output and dominates the export basket, leaving the country acutely exposed to commodity price swings and China's demand cycles. With 86% of exports flowing to a single market, the vulnerability is not just structural but existential. Diversifying productive sectors is not merely desirable — it is a matter of economic survival. It is against this backdrop that the "White Gold" national program carries real strategic weight.

Mongolia sits on one of the world's most valuable natural fiber resources, yet it captures only a fraction of what that resource is worth. Agriculture contributes just 10% of GDP, contracted 8.9% last year while the broader economy grew 7%, and attracted a negligible $1.2 million in foreign investment in 2023. Of all agricultural exports, 95% is cashmere alone. Yet despite this near-total dependence on a single commodity, Mongolia processes only 25% of its raw cashmere domestically. The remaining 75% is simply washed and shipped out as raw fiber, leaving the spinning, weaving, finishing, and the margins that come with them to factories in other countries. Experts estimate that closing this processing gap and selling finished goods instead of raw material could unlock up to $1.5 billion in additional export value annually.

The "White Gold" national program commits ₮2.2 trillion over three years to change this reality. The targets are:

- The domestic processing rate is set to double from 20% to 40%.

- Total production is projected to grow from ₮1.5 trillion to ₮2.3 trillion.

- Cashmere exports are expected to rise from $398 million to $690 million.

- Over 8,200 new jobs are expected to be created across the sector.

The program also covers wool, hide and leather processing, broadening its impact beyond cashmere alone.

The financing structure tells part of the story. The state covers 31.2% of the total cost, with the remainder expected to come through commercial bank lending to individual enterprises. That arrangement places meaningful execution risk on private actors whose appetite for long-term investment in light industry has historically been limited. Banks will lend where they see viable returns, and smaller processors without strong balance sheets may struggle to access the capital the program assumes will flow to them.

In the first week of June 2026, global equity markets were highly volatile. Markets opened the week strongly, with U.S. and Asian equities reaching record highs driven by gains in the technology sector. However, sentiment reversed sharply toward the end of the week after a stronger-than-expected U.S. jobs report increased expectations that interest rates will remain higher for longer. Technology stocks, particularly in the semiconductor sector, came under significant pressure, leading to a broad market decline. European markets remained relatively stable but underperformed amid ongoing geopolitical uncertainty and cautious investor sentiment. Overall, investor sentiment shifted from optimism to caution during the week.

U.S. STOCK MARKET

- S&P 500: -2.62%

- Dow Jones: -0.58%

- Nasdaq: -5.09%

U.S. equity markets had a volatile week, opening strongly but ending sharply lower. All three major indexes reached simultaneous all-time highs on Monday, June 2, with the S&P 500 closing at 7,599.96, the Nasdaq at 27,086.81, and the Dow Jones at 51,078.88, driven by Nvidia's launch of a new AI chip. Markets continued climbing mid-week, with the Dow hitting a record close of 51,561.93 on Thursday, jumping 874 points as investors rotated into non-tech stocks. However, the week ended with a dramatic reversal. On Friday, the Nasdaq lost 5.09% to close at 25,709.43 — its biggest single-day drop since April 2025 — while the S&P 500 fell 2.62% to 7,383.74 and the Dow lost 0.58% to settle at 50,866.78. The catalyst was the May jobs report, which showed payrolls rising by 172,000 — nearly double expectations — effectively eliminating market hopes for Federal Reserve rate cuts in 2026. Disappointment over Broadcom's failure to raise its full-year AI chip outlook also weighed heavily on semiconductor stocks throughout the week.

EUROPEAN STOCK MARKET

- FTSE 100: +0.29%

- STOXX Europe 600: +0.23%

- DAX 40 (Герман): -0.98%

- CAC 40 (Франц): +0.47%

European equity markets were relatively resilient during the week, holding up better than their U.S. and Asian counterparts due to lower exposure to technology stocks. The FTSE 100 gained 0.29% to close at 10,368.05, the STOXX Europe 600 rose 0.23% to 622.66, and France's CAC 40 climbed 0.47% to 8,221.21, while Germany's DAX 40 was the sole decliner, falling 0.98% to close at 24,759.05. Investors remained cautious throughout the week, monitoring developments in the Middle East amid a fragile U.S.-Iran ceasefire and ongoing uncertainty over a resolution to the conflict.

ASIAN STOCK MARKET

- Nikkei 225: -0.06%

- KOSPI: -3.83%

- CSI 300: -1.65%

- SSEC : -0.97%

Asian equity markets closed the week lower across the board. Japan's Nikkei 225 was the most resilient of the region, opening the week at 66,629.6 and closing at 66,588.12, a modest decline of just 0.06%, suggesting that Japanese equities largely weathered the week's global turbulence. South Korea's KOSPI saw the sharpest weekly loss in the region, falling 3.83% from 8,485.67 to close at 8,160.59, likely reflecting the index's heavy weighting toward semiconductor and technology stocks, which came under significant pressure globally following Broadcom's disappointing AI chip outlook and the broader selloff in the tech sector. Chinese markets also ended the week in negative territory, with the CSI 300 declining 1.65% from 4,897.9 to close at 4,816.92, and the SSEC slipping 0.97% from 4,067.16 to 4,027.74, consistent with the cautious global sentiment driven by rising U.S. Treasury yields and fading expectations of Federal Reserve rate cuts in 2026.

⇒ ANTHROPIC FILES FOR IPO AT $965 BILLION VALUATION, OUTPACING OPENAI IN RACE TO PUBLIC MARKETS

On June 1, 2026, Anthropic confirmed it had submitted a confidential draft registration statement on Form S-1 to the U.S. Securities and Exchange Commission, the formal first step toward going public.

The filing came just days after Anthropic closed a $65 billion Series H funding round, pushing its post-money valuation to $965 billion, surpassing rival OpenAI, which was valued at $852 billion following its own record $122 billion raise in late March. Morgan Stanley and Goldman Sachs have been chosen to lead the offering, according to Bloomberg reports.

Anthropic's revenue run rate figure of $47 billion, up from roughly $10 billion just a year ago, is annualized, meaning it is a projection based on current momentum rather than audited booked revenue. Their single biggest growth driver has been Claude Code, Anthropic's AI coding assistant, which became generally available in May 2025 and quickly became a staple for enterprise software teams. Anthropic now counts more than 1,000 business customers spending at least $1 million annually, and eight of the Fortune 10 are Claude customers. Roughly 80% of Anthropic's revenue comes from enterprise clients — compared with around 40% for OpenAI — making its revenue base stickier and more predictable.

One dimension of the Anthropic story that is easy to overlook amid the valuation figures: the company is structured as a Public Benefit Corporation, legally obligated to balance profits with its mission of building AI safely and responsibly. It also has a Long-Term Benefit Trust designed to protect that mission from short-term investor pressure — a governance structure with no real parallel among its peers going public.

⇒ HOW DID THE ISRAEL–LEBANON CEASEFIRE AFFECT THE OIL MARKET?

On June 3 of this year, Israel and Lebanon reached a ceasefire agreement following negotiations held in Washington. This decision had an immediate impact on global oil markets, pulling down prices that had been rising for the previous three consecutive days.

Specifically, the price of Brent crude fell 0.69% to $97.14 per barrel, while WTI crude dropped 0.65% to $95.40 per barrel. In the three days prior to the agreement, oil prices had risen by nearly 10% in total.

Since Iran had stated that it would not make progress in nuclear negotiations with the United States unless the conflict in Lebanon was halted, analysts view this ceasefire as an important step toward advancing talks on Iran's nuclear program and broader regional security issues.

Nevertheless, despite the drop in oil prices, supply-side risks have not fully disappeared. The situation in the Strait of Hormuz remains unstable, and trading warehouse reserves have declined for six consecutive weeks. In the past week alone, reserves fell by 8 million barrels. Such a rapid rate of decline carries the risk of driving oil prices higher again over the longer term.

On another front, fees and costs imposed on Russian oil refineries have risen significantly over the past two years, reaching their highest level compared to the previous year. As a result, the country's budget revenues have been declining, placing additional pressure on its oil export policies.