Weekly market news 03/23/2026

Weekly market news 03/23/2026

- Overview of trading activity on the Mongolian Stock Exchange.

- The Bank of Mongolia kept its policy rate at 12%.

- Industrial output rose by 54% in the first two months of 2026.

- The Bank of England held its policy rate at 3.75%.

- U.S. national debt has surpassed USD 39 trillion.

- Overview of global capital markets.

► MONGOLIAN STOCK EXCHANGE

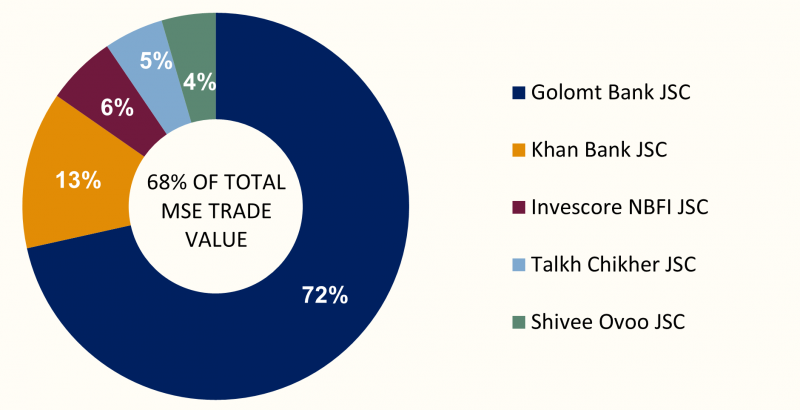

Over the course of the week, a total of 7.6 million securities with a combined value of MNT 6.6 billion were traded on the Mongolian Stock Exchange. In terms of trading value, the most actively traded companies were Golomt Bank JSC, Khan Bank JSC, Invescore NBFI JSC, Talkh Chikher JSC, and Shivee Ovoo JSC. During the same period, two block trades were executed:

- Invescore NBFI JSC (INV) traded 27.1 thousand shares at MNT 9,925 per share, amounting to MNT 250 million in total turnover.

- Golomt Bank JSC (GLMT) saw 1.9 million shares traded at MNT 1,301 per share, generating approximately MNT 2.5 billion in trading value.

Last week, the main indices of the Mongolian Stock Exchange closed lower. The TOP-20 Index declined by 1.51% to 52,006.19 points, while the MSE A Index, which tracks actively traded stocks, fell by 0.83% to 20,101.80 points. Meanwhile, the MSE B Index, representing small and mid-cap companies, decreased by 0.17% to 14,511.05 points, indicating relatively stronger correction movements within that segment. Overall, market activity weakened, with short-term profit-taking dominating investor behavior during the week.

| INDEX | POINTS | WEEKLY CHANGE |

| TOP 20 Index | 52,006.19 | -1.51% |

| MSE A Index | 20,101.80 | -0.83% |

| MSE B Index | 14,511.05 | -0.17% |

⇒ BANK OF MONGOLIA KEEPS POLICY RATE UNCHANGED AT 12%

The Monetary Policy Committee of the Bank of Mongolia convened on March 18 and 20, 2026, and decided to keep the policy rate unchanged at 12%. This decision reflects improvements in the domestic economy, while acknowledging increasing uncertainty in the external geopolitical environment.

Key considerations:

- Inflation: Inflation declined to 6.5% in February 2026, approaching the target range. While price increases for non-food goods and services have moderated, rising food prices continue to exert upward pressure. Risks related to global fuel and food prices may affect the inflation outlook.

- Economic growth: Economic growth improved to 6.8% in 2025, driven primarily by agriculture, mining, and industrial production. In 2026, the mining sector and large-scale projects are expected to support further growth.

- External environment: Improved growth prospects in partner countries, along with high gold and copper prices, have positively impacted trade. However, geopolitical tensions in the Middle East have increased uncertainty and contributed to volatility in commodity prices.

- Although annual inflation has declined toward the midpoint of the target range, ongoing geopolitical developments and unexpected shocks continue to heighten uncertainty and pose risks of rising inflation.

This decision aims to:

- Stabilize inflation at 5% (+/- 2%) starting from 2027.

- Support medium-term macroeconomic stability.

⇒ INDUSTRIAL PRODUCTION SURGES BY 54% IN THE FIRST TWO MONTHS OF 2026

Mongolia’s industrial sector recorded strong growth in the first two months of 2026, with total production reaching MNT 10.4 trillion—an increase of 54%, or MNT 3.6 trillion, compared to the same period last year, according to the National Statistics Office. This growth was mainly driven by intensified mining and extractive activities, along with expansion in certain manufacturing segments.

The mining sector played a dominant role in overall industrial growth, with output rising by 66.8%, or MNT 3.4 trillion. In particular:

• Metal ore mining increased 2.3 times, contributing MNT 2.9 trillion in growth;

• Coal mining rose by 17.3%, or MNT 449.3 billion;

• Additionally, the physical output of copper concentrate, iron ore concentrate, and coal increased by 40.9% to 86.1% compared to the same period last year, further accelerating sector growth.

However, production of some minerals declined, including:

• Unrefined gold

• Fluorspar

• Crude oil

• Silver and zinc concentrates

In the manufacturing sector, the physical output of products such as metal structures, pure alcohol, combed cashmere, lime, vodka, cashmere knitwear, and cement increased by 0.2% to 83.7% year-on-year.

Total industrial sales reached MNT 12.6 trillion in the first two months of the year, marking a 77.3% increase (MNT 5.5 trillion) compared to the same period last year. Of this, mining sector sales alone grew by MNT 5.3 trillion (99.7%).

As one of the key drivers of the economy, the strong performance of the industrial sector signals a positive outlook for Mongolia’s economy in 2026.

Between March 16 and 20, 2026, global financial markets were generally characterized by a cautious sentiment. Geopolitical developments, particularly rising tensions in the Middle East, have increased the risk of renewed inflation through energy markets, thereby influencing investor expectations. At the same time, sector performance remained mixed. Industries such as technology and energy responded differently to market conditions, highlighting divergences across both regions and sectors.

U.S. STOCK MARKET

- S&P 500: -2.52%

- Dow Jones: -2.42%

- Nasdaq: -3.25%

U.S. equity markets closed lower during the period. Market sentiment was weighed down by geopolitical uncertainty—particularly developments in the Middle East—as well as rising inflation risks driven by higher oil prices. At the same time, expectations that monetary policy will remain relatively tight for an extended period dampened investor risk appetite, placing notable pressure on technology and growth stocks in particular.

EUROPEAN STOCK MARKET

- FTSE 100: -3.87%

- STOXX Europe 600: -3.84%

- DAX 40 (Герман): -4.69%

- CAC 40 (Франц): -3.22%

European equity markets experienced broad-based declines, driven by rising energy prices and growing concerns over their impact on inflation and economic growth prospects. In particular, Germany’s DAX Index recorded a steeper drop, reflecting weakened expectations for the future performance of export- and manufacturing-oriented companies. Overall, risk-off sentiment prevailed across the region.

ASIAN STOCK MARKET

- Nikkei 225: -0.48%

- KOSPI: +4.91%

- CSI 300: -3.65%

- SSEC : -3.30%

Asian markets showed mixed performance. Japan’s Nikkei Index declined, weighed down by currency volatility and external uncertainties. Chinese markets also closed lower, reflecting weaker foreign demand and cautious investor sentiment. Meanwhile, South Korea’s KOSPI Index rose, supported by positive expectations in the semiconductor and technology sectors and increased sectoral demand.

⇒ BANK OF ENGLAND HOLDS POLICY RATE STEADY AT 3.75%

The Bank of England decided to keep its policy rate unchanged at 3.75% at its latest meeting. The decision was unanimously supported by all committee members (9–0), marking the first unanimous vote in 4.5 years.

The central bank revised its inflation outlook upward, projecting inflation at 3% for the second quarter and 3.5% for the third quarter.

According to official statements from the Bank of England, the recent escalation of conflict in the Middle East has led to a sharp increase in global energy prices and heightened uncertainty around oil and gas supply stability. These factors have become key drivers of renewed inflationary pressure. As a result, inflation may decline more slowly and could rise again in the short term. Therefore, policymakers consider it premature to begin cutting interest rates at this stage.

Meanwhile, the European Central Bank also kept its policy rate unchanged at 2% and revised its inflation forecast upward from 1.9% to 2.6%.

⇒ U.S. NATIONAL DEBT SURPASSES $39 TRILLION

According to data released by the United States Department of the Treasury on March 17, 2026, total U.S. national debt has reached $39 trillion. This marks the highest level since World War II and represents a much sharper increase than previous growth trends.

The debt has risen by $1 trillion in just five months, driven by a combination of factors including war-related spending, fiscal deficits, and expansionary government policies.

The U.S. has already spent $12 billion on the Iran conflict, with further pressure on the budget expected. In addition, tax cuts, rising defense expenditures, and the high cost of veteran welfare programs are key contributors to the rapid expansion of debt. According to White House economic advisor Kevin Hassett, these costs extend beyond military spending, affecting household economies through rising fuel prices and disruptions in supply stability. These factors are beginning to impact consumption, business costs, and domestic inflationary pressures in the U.S.

Economists view this trajectory as unsustainable, warning that if current trends continue, national debt could reach $40 trillion before the 2026 fall elections. The Government Accountability Office noted that rising debt levels could lead to higher borrowing costs for individuals, increased prices of goods and services, and negative effects on household living standards.