Weekly market news 04/27/2026

Weekly market news 04/27/2026

- Overview of trading activity on the Mongolian Stock Exchange

- Fuel prices, geopolitics, and capital markets: External pressures facing Mongolia’s economy.

- Industrial output rose by 61% in Q1 2026, with mining as the primary growth driver.

- Exports of plant-based products increased, while market concentration remains high.

- Nikkei 225 surpassed the 60,000 level: Driven by leading AI-related stocks.

- Oil prices rose as U.S.–Iran talks collapsed.

- Overview of global capital markets

► MONGOLIAN STOCK EXCHANGE

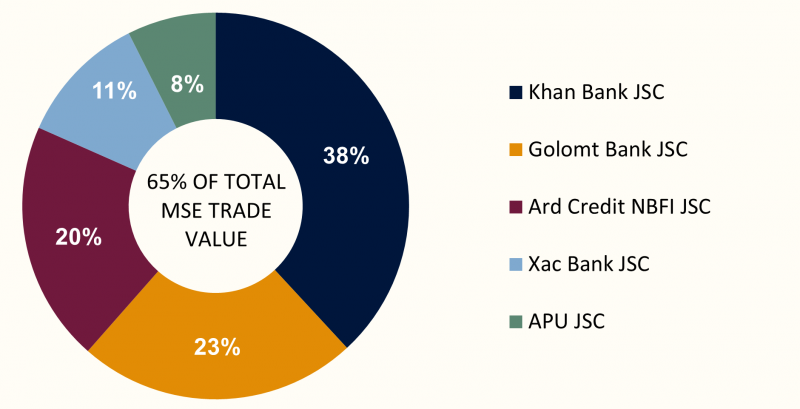

Over the course of the week, a total of 13.25 million securities with a combined value of MNT 6.37 billion were traded on the Mongolian Stock Exchange. In terms of trading value Khan Bank JSC, Golomt Bank JSC, Ard Credit NBFI JSC, XacBank JSC, and APU JSC led market activity, indicating concentration of liquidity in a limited number of actively traded stocks. During the period, a total of 2 block trades was executed:

- Golomt Bank JSC (GLMT) traded 610 thousand shares at MNT 1,240 per share, totaling MNT 756.4 million;

- Ard Credit NBFI JSC (ADB) traded 6.67 million shares at MNT 122 per share, totaling MNT 812.93 million.

Mongolian Stock Exchange indices closed higher over the past week, with positive market sentiment maintained. The TOP-20 Index rose +1.41%, the MSE A Index gained +1.53%, and the MSE B Index increased +0.16%. The gains reflect a continuation of the previous week’s recovery, with buying activity remaining stable. The stronger performance of the MSE A Index indicates relatively solid performance among mid- and large-cap stocks, while the more modest increase in the MSE B Index suggests continued subdued and limited movement in the small-cap segment. Overall, the market appears to be transitioning into a phase of stable short-term growth, with earlier technical factors such as ex-dividend adjustments and seasonal volatility gradually easing.

| INDEX | POINTS | WEEKLY CHANGE |

| TOP 20 Index | 51,318.49 | +1.41% |

| MSE A Index | 19,681.55 | +1.53% |

| MSE B Index | 14,255.85 | +0.16% |

⇒ FUEL PRICES, GEOPOLITICS, AND CAPITAL MARKETS: EXTERNAL PRESSURES ON MONGOLIA’S ECONOMY

At the Cabinet meeting held on April 22, 2026, Prime Minister N. Uchral provided an update on the economic outlook. Rising global oil prices, driven by escalating geopolitical tensions in the Middle East, are beginning to feed into Mongolia’s domestic fuel market.

Domestically, there are emerging conditions for price increases, with regular diesel projected to rise by MNT 2,200 to MNT 5,200, Euro-5 diesel to MNT 5,300, and AI-95 gasoline to MNT 4,100. In response, the government has submitted a draft law to Parliament seeking authority to flexibly adjust import customs duties. However, as of April 23, officials indicated that a sharp immediate increase in fuel prices is not expected.

- Fuel risk: Potential increases in diesel and AI-95 prices could raise production costs across key sectors such as transportation, mining, and agriculture.

- Policy response: The government is pursuing legislative approval to introduce flexible customs tariff mechanisms to manage price volatility.

- MSE outlook: Following a peak in early 2026, benchmark indices may face continued downside pressure.

- Inflation pressure: Higher fuel and energy costs are expected to keep inflation around ~7.0% in 2026.

On the capital markets side, benchmark indices on the Mongolian Stock Exchange, after reaching peak levels earlier in 2026, may face continued downward pressure. Higher fuel and energy costs are expected to keep inflation around 7.0% in 2026, while also increasing input costs for listed companies. This is likely to be reflected in second-quarter earnings, potentially weighing on equity performance.

⇒ INDUSTRIAL OUTPUT SURGES 61% IN Q1 2026, DRIVEN BY MINING SECTOR

According to preliminary data from the National Statistics Office, Mongolia’s total industrial output reached MNT 16.4 trillion in Q1 2026, marking an increase of MNT 6.2 trillion (+61.2% YoY). This represents a significant expansion compared to MNT 8.7 trillion in 2023, MNT 11.7 trillion in 2024, and MNT 10.2 trillion in 2025 for the same period.

The growth was primarily driven by the mining and extractive industries, which recorded output of MNT 13.6 trillion (+74.2% YoY). This was supported by a 2.3x increase in metal ore production (MNT 4.8 trillion) and a 28.0% rise in coal output (MNT 1.0 trillion). On the sales side, total industrial sales reached MNT 18.8 trillion (+75.3% YoY), with metal ore accounting for 62.9% of export sales.

Key highlights:

- Approximately 94% of total growth was driven by the mining sector, underscoring continued concentration risks.

- Copper concentrate output (metal content) increased 36.4% to 611 thousand tons.

- Coal production rose 68.7% to 25.7 million tons, reinforcing its role as a key export commodity.

- Cement production grew 96.7% to 171 thousand tons, indicating rising demand from construction and infrastructure investment.

- The food and beverage segment weakened, with beverages down 18.2% and meat production declining 62.3%, signaling softness in certain domestic sectors.

- The industrial production volume index declined 14.1% YoY to 214.0 (2015=100) in March 2026.

While headline growth remains strong, it is largely concentrated in mining. The decline in the physical volume index suggests that nominal growth is being driven more by price effects than by real output expansion. As such, inflation-adjusted performance remains more moderate, and investors should differentiate between nominal and real growth dynamics when assessing the sector.

⇒ EXPORTS OF PLANT-BASED PRODUCTS INCREASE, WITH HIGH MARKET CONCENTRATION PERSISTING

Over the past year, Mongolia’s exports of plant-based products reached 183.5 thousand tons, maintaining a steady growth trajectory. 86% of total exports were directed to China, indicating that market concentration remains high.

In terms of structure, 75% of exports consisted of cultivated crops, 24% processed products, and the remaining 1% wood materials. Rapeseed, feed bran, and hay accounted for the majority of cultivated exports, including 100.8 thousand tons of rapeseed, 27.9 thousand tons of bran, 23.7 thousand tons of feed hay, and 10.8 thousand tons of potatoes. Smaller volumes included products such as sea buckthorn, carrot juice, and pine nuts.

The growth in exports has contributed to increased activity in the agricultural sector, supporting crop diversification, improved soil fertility, and higher yields. At the same time, the high concentration in a single export market continues to pose a structural risk.

Overall, while export growth is supporting the performance of the agricultural sector, further progress in market diversification and value-added processing remains an important factor for sustainable development.

During the week of April 21–25, 2026, global equity markets reflected a mixed and divergent dynamic, shaped by the interplay between geopolitical developments and corporate earnings releases. The expiration of the U.S.–Iran ceasefire and ongoing disruptions in the Strait of Hormuz placed particular pressure on European markets, reinforcing expectations of higher energy costs and renewed inflationary pressures. At the same time, regional performance diverged, with U.S. markets showing mixed movements, Europe experiencing broad-based declines, and Asia demonstrating relatively strong recovery. This indicates that market trends remain uneven, driven by differences in macro conditions, sector composition, and investor risk assessments rather than a synchronized global direction.

U.S. STOCK MARKET

- S&P 500: +0.67%

- Dow Jones: -0.39%

- Nasdaq: +1.72%

In the U.S. market, index performance was mixed, with the Nasdaq’s gains reflecting sustained demand for technology and growth stocks. In contrast, the decline in the Dow Jones indicates relatively weaker performance in industrial and traditional sectors. Broad-based gains were not evident, as selective buying dominated and investors remained concentrated in specific segments. Ongoing uncertainty around interest rate expectations and the inflation outlook also continued to limit a more uniform upward movement across indices.

EUROPEAN STOCK MARKET

- FTSE 100: -2.17%

- STOXX Europe 600: -0.90%

- DAX 40 (Герман): -2.32%

- CAC 40 (Франц): -1.88%

European markets saw broadly distributed declines, with a more pronounced correction following the previous period of gains. The pullback in the DAX 40 and FTSE 100 reflects pressure on industrial and export-oriented companies. In addition, ongoing uncertainty around regional growth prospects, inflation, and the direction of monetary policy supported a more cautious investor stance, reinforcing risk-off positioning.

ASIAN STOCK MARKET

- Nikkei 225: +2.12%

- KOSPI: +6.86%

- CSI 300: +0.86%

- SSEC : +0.70%

Asian markets recorded broadly positive performance, led by a +6.86% gain in the KOSPI, driven by a recovery in technology and export-oriented sectors. Japan also posted solid gains, while Chinese markets showed more modest, stable increases, reflecting ongoing caution amid domestic economic conditions. Overall, the impact of external risks appeared relatively contained, with domestic policy factors and sector fundamentals playing a more prominent role in shaping market performance during the week.

⇒ NIKKEI 225 SURPASSES 60,000 LEVEL: AI-DRIVEN RALLY LED BY CHIP AND TECH STOCKS

During Thursday’s session on the Tokyo Stock Exchange, the Nikkei 225 index reached 60,013.98, surpassing the 60,000 mark for the first time since its inception in 1950. The milestone was driven by strong gains in AI- and semiconductor-related stocks, including SoftBank Group (+6.4%), Advantest (+2.65%), Tokyo Electron (+1.76%), and Fujikura (+0.65%).

However, the rally proved short-lived as profit-taking emerged shortly after the record high. The index closed at 58,952.11, down 1.06%, while the broader TOPIX index declined 0.76% to 3,716.38. Market breadth remained weak, with only 23% of listed companies advancing and 72% declining, indicating that the gains were concentrated in a narrow segment of the market.

Key drivers:

- SoftBank Group (+6.4%): Gains were supported by announcements related to AI chip development by its subsidiary Arm Holdings, as well as increased investment in AI robotics.

- Advantest (+2.65%), Tokyo Electron (+1.76%): Strength in Japan’s semiconductor sector followed upward revisions in demand outlooks by global players such as ASML and TSMC.

- U.S.–Iran ceasefire extension: Reports of an indefinite extension mediated by Pakistan supported early-session risk sentiment.

In recent months, Japanese equities have benefited from increased foreign inflows, relatively accommodative monetary policy, and improvements in corporate governance. The technology sector, in particular, has driven the sharp upward momentum. However, the pace of gains has raised concerns over elevated valuations, prompting a late-session correction. At the same time, renewed geopolitical tensions in the Middle East—particularly reports of vessel detentions in the Strait of Hormuz—pushed oil prices higher and increased risk aversion. This contributed to a stronger U.S. dollar, with the exchange rate reaching approximately JPY 159 per USD, adding further pressure on investor positioning.

⇒ OIL PRICES RISE AS U.S.–IRAN TALKS COLLAPSE, HEIGHTENING MARKET UNCERTAINTY

Global oil prices moved higher following the cancellation of a planned second round of U.S.–Iran negotiations in Pakistan, reinforcing geopolitical risk concerns across energy markets.

According to market data, Brent crude futures for July delivery rose 2.30% to $101.41 per barrel, while WTI crude for June delivery increased 2.15% to $96.43 per barrel after trading opened. The price movement reflects heightened sensitivity to supply risks linked to escalating tensions in the Middle East.

U.S. President Donald Trump confirmed over the weekend that the delegation’s planned visit to Islamabad had been cancelled. He later stated that Washington had received a new proposal from Tehran under more favorable terms. However, Iranian officials maintained that no formal meeting with U.S. representatives had been scheduled, signaling a lack of alignment between the two sides.

Iranian President Masoud Pezeshkian, in a phone call with Pakistan’s Prime Minister Shehbaz Sharif, emphasized that Iran would not engage in negotiations under conditions of pressure, threats, or ongoing maritime restrictions. Tehran has continued to push back against U.S. actions, particularly those affecting its ports and access to international trade routes.

The breakdown in talks comes at a time when the Strait of Hormuz—responsible for roughly 20% of global oil shipments—remains a key point of concern. Any disruption or perceived risk to this critical chokepoint has immediate implications for global energy supply expectations and price volatility.

Market participants are increasingly pricing in geopolitical risk premiums, with oil markets reacting not only to actual supply disruptions but also to shifts in diplomatic developments. The latest escalation adds to existing concerns over inflation, as rising energy prices are likely to feed through into broader cost structures globally.

Overall, the failure to advance negotiations underscores continued uncertainty in the geopolitical landscape, with energy markets remaining highly sensitive to developments in U.S.–Iran relations and broader Middle East dynamics.