Weekly market news 04/13/2026

Weekly market news 04/13/2026

- Overview of trading activity on the Mongolian Stock Exchange

- Inflation Accelerates Again in March, Reaching 7.3%

- Mongolia’s Economic Growth: Strong Start to the Year and the Medium Term Outlook

- Trade Finance Forum Held

- Geopolitical Tensions Ease, Markets Breathe a Sigh of Relief

- Samsung Electronics: AI Chip Demand Drives Sharp Profit Surge

- Overview of global capital markets

► MONGOLIAN STOCK EXCHANGE

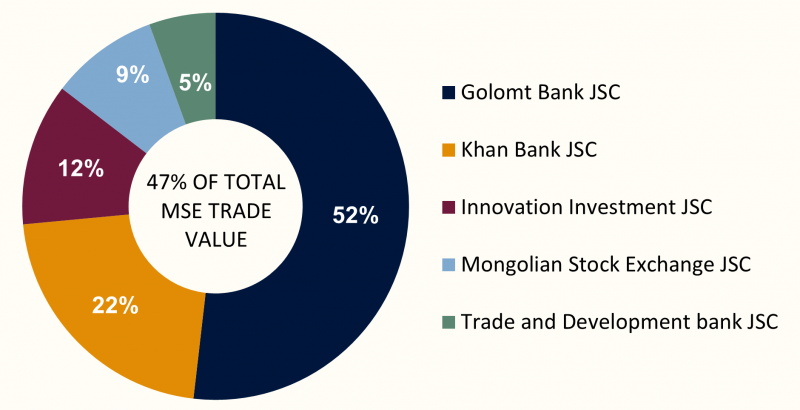

Over the course of the week, a total of 7.4 million securities with a combined value of MNT 6.4 billion were traded on the Mongolian Stock Exchange. In terms of trading value, Golomt Bank JSC, Khan Bank JSC, Innovation Investment JSC, Mongolian Stock Exchange JSC, and Trade and Development bank JSC led market activity, indicating concentration of liquidity in a limited number of actively traded stocks. During the period, a total of one block trade was executed:

- Golomt Bank JSC (GLMT): 498 thousand shares at MNT 1,245, totaling MNT 620 million

Mongolian Stock Exchange indices closed the week lower, reflecting a broadly weaker performance across the market. The TOP-20 Index declined by -1.27% to settle at 50,119.16 points, while the MSE A Index fell -0.69% to 19,005.34 points. The MSE B Index recorded the sharpest decline, retreating -2.26% to 14,159.61 points, indicating relatively higher selling pressure among small- and mid-cap stocks. The more pronounced drop in the MSE B Index suggests increased risk aversion toward less liquid securities, while the comparatively modest decline in the MSE A Index points to relative resilience among larger, more actively traded companies. Market movements during the week were largely driven by seasonal and technical factors rather than any deterioration in underlying fundamentals. The commencement of ex-dividend trading for several listed companies led to mechanical price adjustments in line with dividend payouts. In addition, the announcement of annual general meeting (AGM) schedules and the initiation of shareholder registration periods influenced short-term investor positioning and trading activity.

Overall, the weekly weakness in the indices appears to reflect dividend-related price adjustments and internal market dynamics, rather than systemic risk. Investor sentiment remained cautious, with selective profit-taking and repositioning ahead of corporate action events shaping market performance.

| INDEX | POINTS | WEEKLY CHANGE |

| TOP 20 Index | 50,119.16 | -1.27% |

| MSE A Index | 19,005.34 | -0.69% |

| MSE B Index | 14,159.61 | -2.26% |

⇒ INFLATION ACCELERATES AGAIN IN MARCH, REACHING 7.3%

In March 2026, the consumer price index (CPI) rose to 7.4% nationwide, accelerating by 1.2 percentage points from the previous month. The uptick in inflation was driven mainly by higher fuel prices and increases in food prices.

Due to ongoing geopolitical instability in the Middle East, prices for fuels other than AI 92 increased, creating upward pressure on transportation and logistics costs. At the same time, rising prices of meat and meat products are contributing to persistent inflationary pressures. Nationwide, prices in the food category increased by 13.9–15.2% year on year, indicating that food items remain the dominant component of inflation. In particular, meat and meat products rose by 23% compared to the same period last year, making the largest contribution to overall inflation. This increase may be linked to seasonal supply constraints, higher transportation costs, and import related factors.

Inflation in Ulaanbaatar also accelerated in March, increasing by 1.5% month on month and 7.3% year on year. The main driver of inflation in the capital was likewise the rise in food prices, with the food category increasing by 15.3% in March, the highest level since September 2023. Experts warn that if fuel and meat prices remain elevated, inflation is likely to continue intensifying in the coming months.

⇒ MONGOLIA’S ECONOMIC GROWTH: STRONG START TO THE YEAR AND THE MEDIUM TERM OUTLOOK

Mongolia’s economy posted strong growth in the first two months of 2026, supported by increased activity in the mining sector and seasonal factors. According to preliminary data from the National Statistics Office, real GDP grew by 7.6% year on year, driven mainly by a 32.3% increase in value added from mining and extraction and a 4.2% expansion in the services sector. As a result, the economy grew by 8.6% in January and 7.6% in February, reflecting robust momentum at the start of the year.

However, the World Bank’s latest Mongolia Economic Update notes that after the sharp rebound recorded in 2025, economic growth is expected to moderate to around 5.0% in 2026. In the previous year, the ramp up of copper production at Oyu Tolgoi, along with a rapid recovery in the livestock sector following severe weather related losses, helped offset slower coal exports and subdued foreign investment, pushing overall growth to 6.9%. As these one off factors return to more normal levels in 2026, overall growth is expected to slow.

Looking ahead, steady domestic demand and spending under government led projects and programs are likely to remain key pillars supporting economic activity. Nonetheless, the World Bank warns that external risks—including geopolitical uncertainty, trade tensions, and volatility in global commodity prices—could adversely affect the growth outlook. It also highlights that as major mining projects move beyond their core construction phases, foreign direct investment is likely to slow, while private investment may remain constrained in the near term.

On the domestic front, a looser fiscal stance could provide short term support to growth but may also intensify inflationary pressures and widen the current account deficit. This could, in turn, necessitate the continuation of tight monetary policy. Against this backdrop of elevated macroeconomic pressures, the World Bank projects that inflation will remain relatively high throughout 2026, averaging around 8.5%.

⇒ TRADE FINANCE FORUM HELD

Attention within Mongolia’s financial sector is increasingly shifting away from traditional lending growth toward export and trade finance, as banks look to support sectors that generate foreign currency earnings through lower risk, cash flow based financing solutions.

Against this backdrop, the Trade Finance Forum organized by Trade and Development Bank of Mongolia was held last week under the theme “Resource Economy.” The forum discussed trends in financing natural resources, energy, and international trade, as well as ways to reduce financing costs. Discussions focused on practical solutions to enhance clients’ competitiveness through tailored banking products and services.

Globally, rapid technological advancement, the expansion of renewable energy, and the rise of an economy driven by artificial intelligence are reshaping demand for natural resources. As a result, demand for strategic metals such as copper, lithium, and rare earth elements is expected to increase by 30–40% by 2030. While this creates significant opportunities for resource rich countries, experts emphasized that effective financing mechanisms, trade frameworks, and policy coordination remain essential to translating these opportunities into tangible economic returns.

For Mongolia, the mineral resources sector continues to serve as a core pillar of economic growth, underscoring the growing need for a more stable and efficient system of trade and financing. As of 2025, Trade and Development Bank accounted for 32% of total mining sector financing within the banking system. Of this total, 60.7% was allocated to gold mining, 19.6% to coal, 12.3% to iron ore, and the remaining 7.4% to other mineral projects, including silver, non ferrous metals, oil, uranium, and thorium. This distribution highlights a gradual diversification of financing within the sector.

Overall, market participants view the growing activity in trade finance as an early but concrete signal that financial level support for non mining exports is beginning to take shape.

On a weekly basis, global equity markets posted a broadly positive rebound, with major indices closing higher across most regions. Gains were relatively strong in the U.S. and European markets, while Asian markets were generally positive but showed divergent performance across countries and sectors, indicating that investor strategies continue to differ by region.

U.S. STOCK MARKET

- S&P 500: +3.48%

- Dow Jones: +3.11%

- Nasdaq: +4.03%

U.S. equity markets delivered a positive performance throughout the week, with major indices closing higher, signaling a renewed risk on sentiment among investors. All key benchmarks recorded solid gains, reflecting improved market confidence. The S&P 500 rose 3.48%, Nasdaq advanced 4.03%, and the Dow Jones Industrial Average climbed 3.11%. The strong performance appears to be driven by easing concerns over macroeconomic uncertainty and stabilizing expectations around corporate earnings. In particular, Nasdaq’s outsized gains highlight a recovery in growth oriented and technology stocks, which led market performance over the week.

EUROPEAN STOCK MARKET

- FTSE 100: +1.57%

- STOXX Europe 600: +2.81%

- DAX 40 (Герман): +2.68%

- CAC 40 (Франц): +3.27%

European markets recorded broad based gains, with all major regional indices delivering strong performances. The DAX 40 rose by 2.68%, STOXX Europe 600 advanced 2.81%, CAC 40 climbed 3.27%, and FTSE 100 increased by 1.57%. The rally in European markets was supported by positive momentum in global markets and more stable expectations regarding the region’s economic outlook, both of which helped underpin investor confidence. In particular, the strong performance of the broad based STOXX Europe 600 index signals an overall improvement in market sentiment across the region.

ASIAN STOCK MARKET

- Nikkei 225: +6.99%

- KOSPI: +8.03%

- CSI 300: +4.29%

- SSEC : +2.63%

Asian equity markets delivered strong gains last week, with investor risk appetite picking up across the region. All major indices advanced, reflecting positive external influences and improving regional economic expectations. Japan’s Nikkei 225 surged 6.99%, led by export oriented and technology stocks. South Korea’s KOSPI posted the strongest performance in the region, rising 8.03%, as demand increased for semiconductor and high technology shares. In China, the CSI 300 gained 4.29%, while the Shanghai Composite Index (SSEC) rose 2.63%, supported by policy stimulus measures and rising participation from domestic investors. The rally in Asian markets was underpinned by positive momentum in U.S. and European markets and strengthening confidence in the regional economic outlook. In particular, the strong performance seen in Japan and South Korea is viewed as a signal that the global technology sector cycle may be entering a renewed recovery phase.

⇒ GEOPOLITICAL TENSIONS EASE, MARKETS BREATHE A SIGH OF RELIEF

Global financial markets experienced a measure of relief after armed conflict in the Middle East narrowly gave way to a temporary ceasefire agreement. The reopening of the Strait of Hormuz helped ease short term risks to energy supply, sharply reducing price pressures in the oil and gas markets. With the parties agreeing to a two week ceasefire, the immediate risk of further escalation declined, allowing markets to avoid what many had feared could be a worst case scenario. While the agreement creates space for longer term peace talks, analysts caution that underlying tensions remain unresolved, keeping uncertainty elevated.

Markets reacted most visibly in the energy sector. Brent crude prices fell by as much as 16% in a single day, settling near USD 95 per barrel, while European natural gas futures dropped by more than 20%, marking the steepest decline in nearly two years. This sharp correction in energy prices fueled expectations that inflationary pressures may ease in the near term.

As risk sentiment improved, investors rotated out of safe haven assets and back into bonds, technology stocks, and AI related equities. The U.S. dollar weakened, equity indices across the Asia Pacific region rebounded to levels seen in early March, and Bitcoin climbed to a three week high.

Overall, markets spent the past week temporarily stepping back from heightened geopolitical risk, signaling a revival in risk appetite. However, with the ceasefire remaining short term in nature, geopolitical uncertainty continues to represent a key risk factor for markets.

⇒ SAMSUNG ELECTRONICS: AI CHIP DEMAND DRIVES SHARP PROFIT SURGE

Samsung Electronics (005930.KS) significantly outperformed market expectations in the first quarter of 2026, reporting an operating profit of KRW 57.2 trillion, up 755% year on year. The strong performance was driven primarily by a surge in demand for artificial intelligence–focused chips, while revenue increased by 68% year on year to KRW 133 trillion. Notably, operating profit for the quarter exceeded the company’s total profit for full year 2025, drawing strong attention from investors.

Rising orders for high speed memory chips used in cloud computing and data centers lifted profitability in Samsung’s semiconductor business, allowing chip related earnings to surpass those from the smartphone segment. Analysts highlighted that demand for AI chips remained resilient despite heightened geopolitical uncertainty in the Middle East.

Following the release of the earnings report, Samsung Electronics shares rose 1.8% to close at KRW 196,500, with intraday gains reaching as high as 5%.

Meanwhile, another major development drew market attention as a member of the founding family sold 15 million shares worth KRW 3.1 trillion, marking one of the largest block trades in South Korean stock market history. The transaction was reportedly executed to cover inheritance taxes and other financial obligations, with several major international investment banks acting as underwriters—an indication that overall market confidence remains relatively stable.